Tactical to Practical: Understanding the Importance of Types of Market Declines

February 14, 2020 |

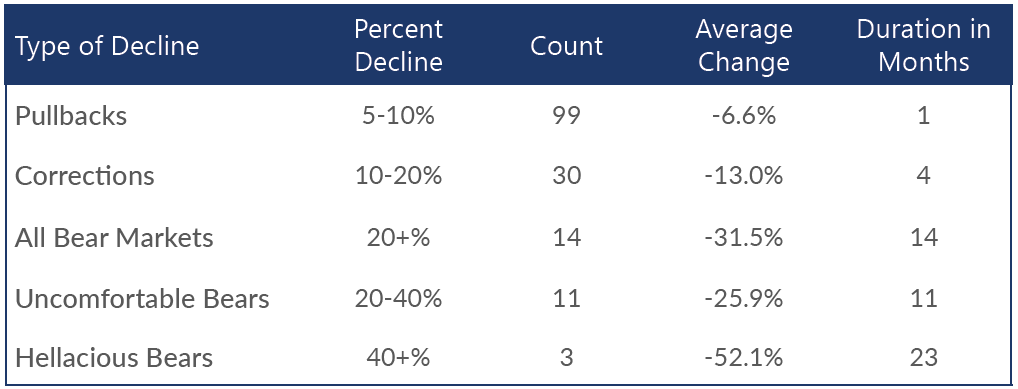

Most investment professionals would agree that stock market price movement in the 0-5% range is just ordinary market movement or statistical “noise”. After this, there are three types of market declines that are simply distinguished by the size of the declines: A Pullback is defined as a 5-10% drop, a Correction is a 10-20% decline and a Bear Market is a 20+% decrease in market price. The first should be ignored as it is also ordinary market movement. The second two should be avoided.

Breaking Down Market Declines

Five to ten percent pullbacks are a common occurrence in the equity markets. During the cyclical bull markets since World War II, there have been 98 pullbacks—13 during the 1990s bull, 12 during the 2002-2007 bull and 18 during the current bull market. On average, there have been three pullbacks each bull market year and the 2009-2016 period was no exception. However, since November of 2016 when we experienced a whopping 5.02% decline in the S&P 500® Index, the U.S. equity markets enjoyed over a year of remarkably low volatility and virtually no pullbacks greater than 3.3%. This anomaly continued into 2018, but was eventually shattered by a -10.16% market correction in February. Now that “normal” volatility is back (relative to its historical range), will we see the average three pullbacks per year return? Perhaps.

S&P 500® Index Price Declines (Excluding Dividends): 1946-August 2019

Source: Bloomberg, Beaumont Capital Management. Data as of 8/31/2019.

Despite the hype assigned by the financial media, Pullbacks are normal market action, Pullbacks are healthy for the markets, and Pullbacks should not be reacted to nor acted upon. If an investor cannot handle a 10% decline in their portfolio, it can be argued they do not belong in equities. Setting proper client expectations is paramount and not reacting to ordinary Pullbacks should be at the top of the list.

Why the Interest in Pullbacks?

Over the last decade, reacting to Pullbacks has helped cause or contributed largely to the under-performance and even the undoing of more than a dozen tactical managers. We believe that no tactical strategy is able to successfully avoid ordinary 5-10% Pullbacks and provide timely reinvestment without being subject to whipsaw. Whipsaw occurs when the price of a security heads in one direction, but is quickly followed by a movement in the opposite direction. The term’s origin is from the push and pull action used by two lumberjacks to saw wood with a large, two-handled saw.

Pullbacks Tend to be Short with Steep Slopes

The chart below illustrates an example of this. Let’s say we are experiencing a Pullback that will bottom at the historical average of -7%. The first 5% decline simply alerts the manager that the market is in a Pullback. Then, the strategy only has between -5% to -7% of additional decline to react (sell) if the strategy is to “avoid” any of the Pullback. If a manager successfully gets out of the market before the bottom, he then has less than 1-2% of the initial recovery to reinvest without incurring a loss.

Source: Bloomberg, Beaumont Capital Management. Data as of 8/31/2019.

However, based on the historical data back to World War II, an interesting phenomenon occurs when we exceed a 10% Pullback and delve into a Correction. The average loss doubles and the average length almost quadruples. The realities of investment math begin to have a greater effect as the larger a loss a portfolio sustains, the harder the remaining capital has to work just to break even. Between a 10% and a 15% decline is the time to evaluate the situation and to look to sell the weakest positions in a portfolio, even if it means raising cash. Furthermore, when they are occurring, no one knows how far these types of Corrections will go. As the “S&P 500 Index Price Declines” chart above shows, in addition to the 30 Corrections, 14 additional declines led to full-fledged Bear Markets with even more devastating results. Very quickly we switch from ignore to implore… and a rules-based investment system can be engineered to provide this type of distinction and react only when necessary.

Growth Strategies with Defensive Capabilities

The lesson? Stock markets are cyclical and are subject to frequent moves of plus or minus 10%. Since Pullbacks occur with frequency and consistency, tactical strategies that avoid reacting to Pullbacks can have a distinct advantage. In fact, not reacting to common Pullbacks in bull markets has proven to be the better course of action from a performance, turnover and expense standpoint since 1946. It is not the ordinary Pullbacks that devastate a portfolio; it is the large losses found in Corrections or Bears that hinder long term success.

Why Not Buy and Hold?

If we are in a complete vacuum, if the investor has no emotions, an unlimited time-frame, vast wealth and/or no need for the money, then yes, historically it makes sense to buy and hold. Yet as every advisor knows, this most often is not the case. DALBAR proves this every year in their Annual Investor Behavior Report, where they show how the average investor only receives about 1/3 of the market’s return over time. Why?

Humans are emotional. We invest to improve our futures. Corrections and Bear Markets illicit fear that our futures will be irreparably harmed or that a major goal may be destroyed or significantly delayed. It makes sense that investors react…but doing so too soon, as outlined above, is even more harmful. Investors, driven by human emotion, cannot help themselves and they sell at the worst possible times.

Investors and advisors need growth strategies that can make the buy and sell decisions for them using a rules-based system. Remove emotion from the investment process. Smooth the investor experience by embracing our clients’ humanity and acknowledging how they feel and act. In short, deliver what investors need… and Deliver What Investors Expect®.

Sources and Disclosures: