Energy Sector Runs Out of Steam, Tanking Business Activity in China, Yield Curve Inverts Again

February 21, 2020 | FIRESIDE CHARTS

While the S&P 500 has remained fairly “energized” throughout recent periods of geopolitical and epidemiological uncertainty, the index’s energy sector has failed to live up to its name for quite some time now. The broad Energy Select Sector SPDR ETF (a.k.a XLE—though good luck googling it…) is down nearly 20% over the trailing 12 months, and U.S. energy stocks haven’t underperformed the S&P 500 by this wide a margin in nearly 80 years. The coronavirus hasn’t helped matters; flight cancellations just topped 200,000 and sent jet fuel prices to 2+ year lows. The epidemic has sparked a surge in the USD as investors search for safety, but could that strength complicate matters for our other major economic threat—the trade war with China? Negotiations may be relegated to the back burner for the moment as China faces tanking business activity, growth, and productivity that could spell disastrous news for small and medium businesses without the resources to withstand a significant supply chain disruption. Unsurprisingly, the USD isn’t the only safety asset in high demand; yields are plummeting as investors pile into long-term treasuries and it’s sparked yet another yield curve inversion. Remember when those made headline news? Finally, Tesla’s runup has been one for the record books, but has investor interest (and optimism) risen too high?

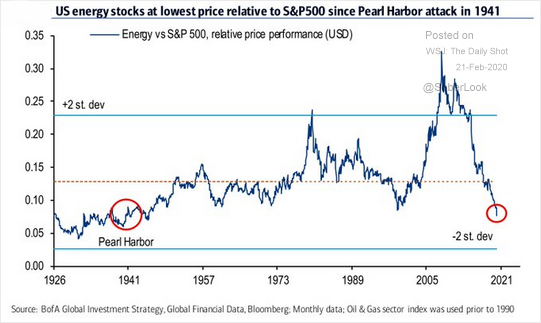

1. The SPDR S&P 500 Energy Sector ETF has realized a negative total return over the past 3 and 5 years during a raging bull market.

Source: WSJ Daily Shot, from 2/21/20

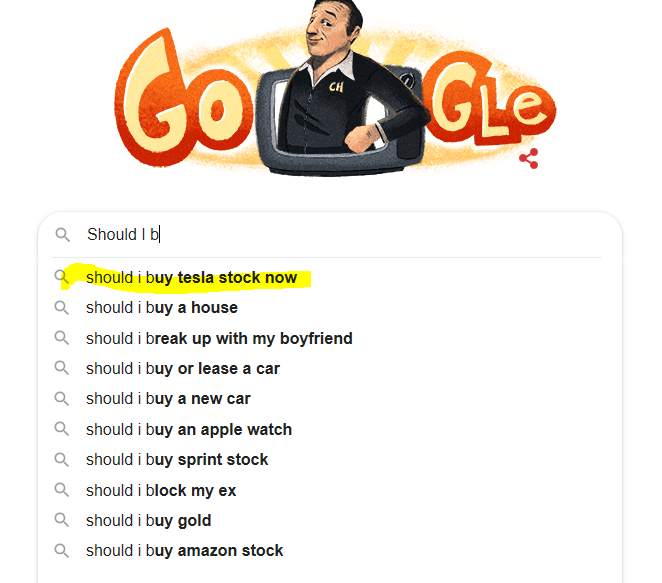

2. Another unscientific gauge of sentiment surrounding the energy sector:

Source: Google, as of 2/21/20

3. The coronavirus flight to safety is at least partially responsible for the USD’s latest surge…

Source: WSJ Daily Shot, from 2/20/20

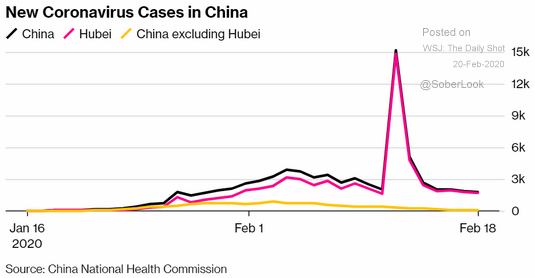

4. The spike a few days ago was due to counting methodology. It appears the virus is coming under control.

Source: WSJ Daily Shot, from 2/20/20

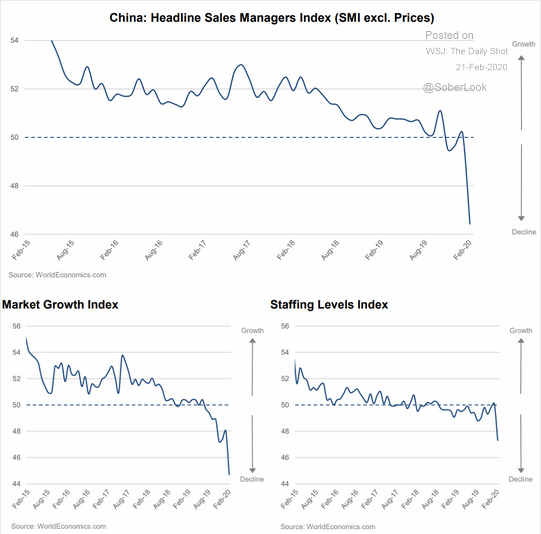

5. China’s economy is grinding to a halt. If this continues for long enough it will have a major impact on global supply chains.

Source: WSJ Daily Shot, from 2/21/20

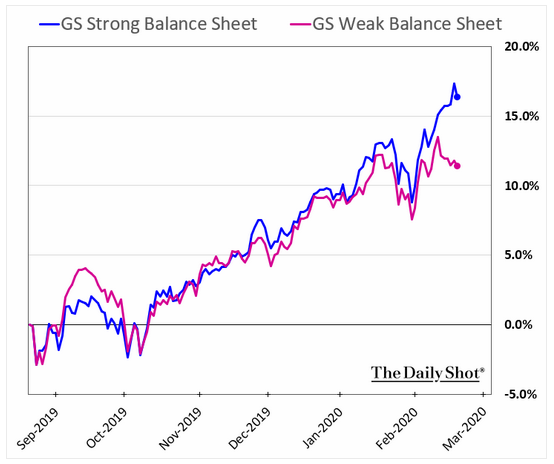

6. An extended supply chain disruption could be very bad for companies without the financial flexibility to manage through.

Source: WSJ Daily Shot, from 2/21/20

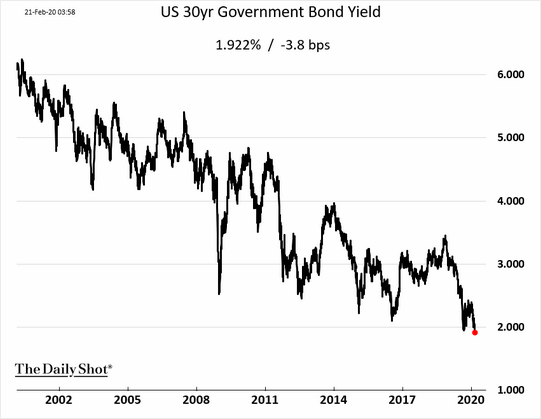

7. Long bond yields have continued to plummet.

Source: WSJ Daily Shot, from 2/21/20

8. And the yield curve has inverted again.

Source: WSJ Daily Shot, from 2/21/20

9. Tesla’s recent surge has certainly captured investors’ attention. Is that a good thing?

Source: Google, as of 2/21/20

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.