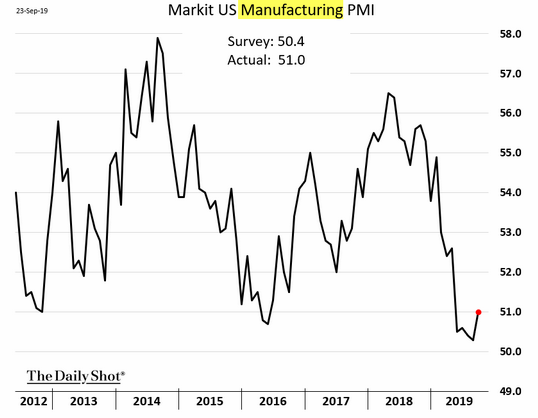

U.S. Manufacturing at 5-month High as Europe Contracts, a Look at Market Effects of Stimulus

September 27, 2019 | FIRESIDE CHARTS

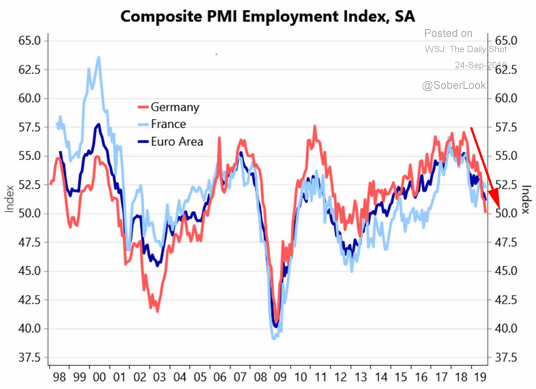

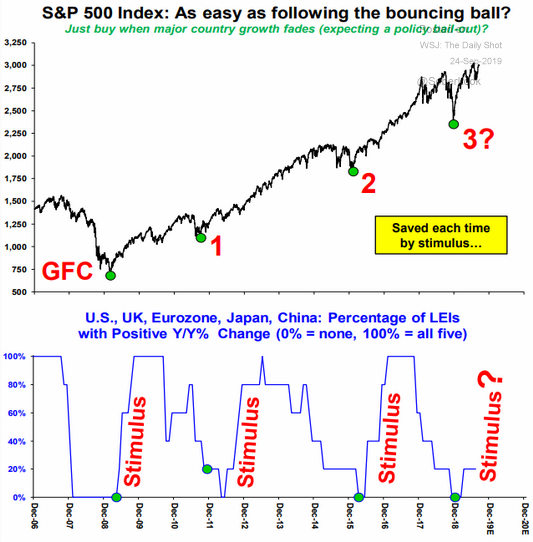

Employment indices are softening in Europe as it ventures deeper into manufacturing contraction, helmed by Germany which saw its manufacturing PMI decline at it’s fastest pace in a decade (re: since the recession era). We’ve already seen the yield curve invert; is this another signal of impending recession? Stateside manufacturing, however, ticked up slightly this month, beating expectations at a print of 51.0, hitting a five-month high, and managing to cling to growth. Could the Fed’s July “mid-cycle adjustment” be to thank? We can see below the effect of government stimulus on the S&P 500 and LEIs… but this pattern can’t be sustainable, can it?

1. After an inverted yield curve, the best predictor of a pending recession is rising unemployment. This new trend does not bode well…

Source: Nordea & Macrobond, as of 9/24/19

2. The good news and the bad news…

Source: WSJ Daily Shot, as of 9/24/19

3. So what happens if the stimulus stops or is not enough? We live in a cyclical economic system and messing with it may not end so well…

Source: Bloomberg & Stifel, as of 9/24/19

4. As a reminder, the trade war started around May of 2018.

Source: Bloomberg, as of 9/23/19

5. The U.S. manufacturing sector is fighting hard to stay in growth mode.

Source: WSJ Daily Shot, as of 9/24/19

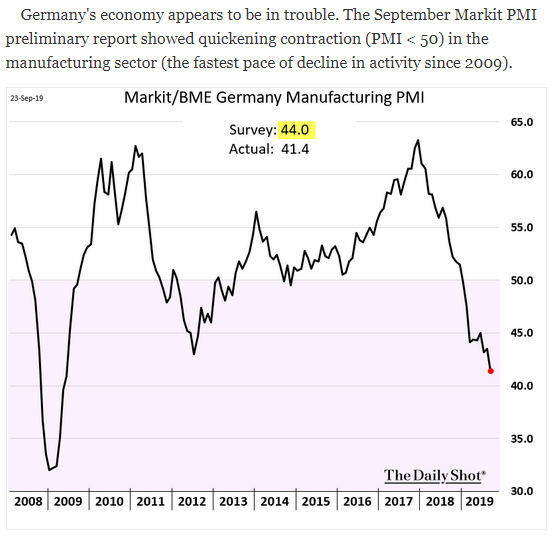

6. The global trend for manufacturing is still down. Germany is a casualty of the trade war… the world’s 4th largest economy having to contend with #1 and 2…

Source: WSJ Daily Shot, as of 9/24/19

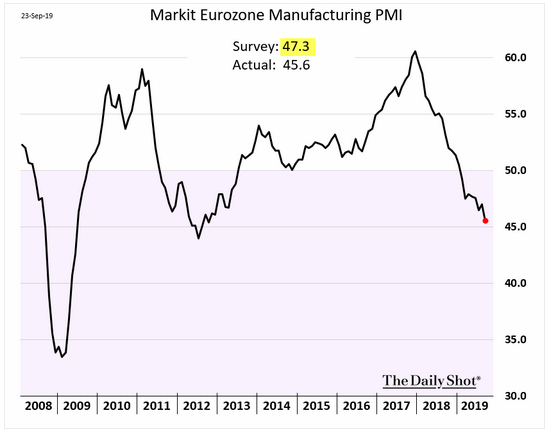

7. Here is Europe as a whole; readings below 50 indicate contraction…

Source: WSJ Daily Shot, as of 9/24/19

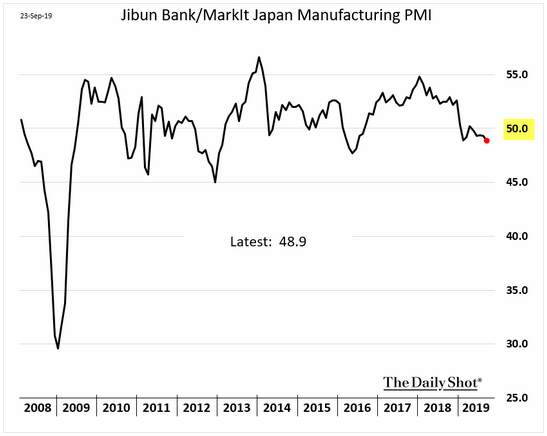

8. Japan remains in a manufacturing contraction…

Source: WSJ Daily Shot, as of 9/24/19

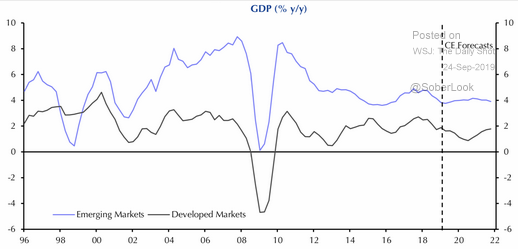

9. The GDP growth rate of emerging markets is still double that of the developed international markets

Source: Capital Economics, as of 9/24/19

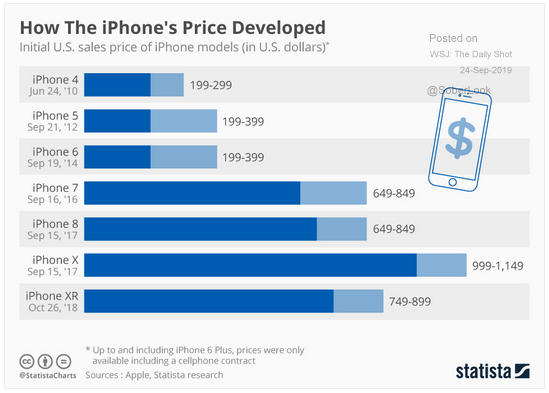

10. There is a limit to what people will pay for a phone!

Source: Statista, as of 9/24/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.