BCM 1Q20 Market Commentary: To V or Not to V, That Is the Question…

April 7, 2020 | COMMENTARY

With apologies to Mr. Shakespeare…

The Covid-19 pandemic has set upon the globe with lightning speed and is unlikely to leave us anytime soon. First and foremost, we hope that you, your family and loved ones are well. While the level of disruption that the virus has caused to our daily lives is unprecedented, we wish to offer hope with a healthy dose of realism.

As confirmed global infections surged past three-quarters of a million people on April 1st, we are reminded of the importance of staying home, incessantly washing our hands, and setting proper social distancing if we must venture out. Unfortunately, the inconsistent spread and response across our country will only delay victory. Different states and municipalities will enter lockdown while others delay or prematurely emerge, potentially spreading the infection anew. This timing and coordinated response issue is likely to compound exponentially with the rest of the world involved. However, this is the United States of America, and betting against us has never been a good idea. It may take more time, economic writhing and pain before any semblance of normalcy returns but with resolve, determination and compassion, we can end this pandemic.

Moving on to the markets, the first quarter of 2020 was historic. The list of extraordinary, if not record-setting, events includes:

- The fastest bear market ever, taking roughly half the time of 1987. Since WWII, the average bear took 8 months to unfold, this one took, so far, less than one month.

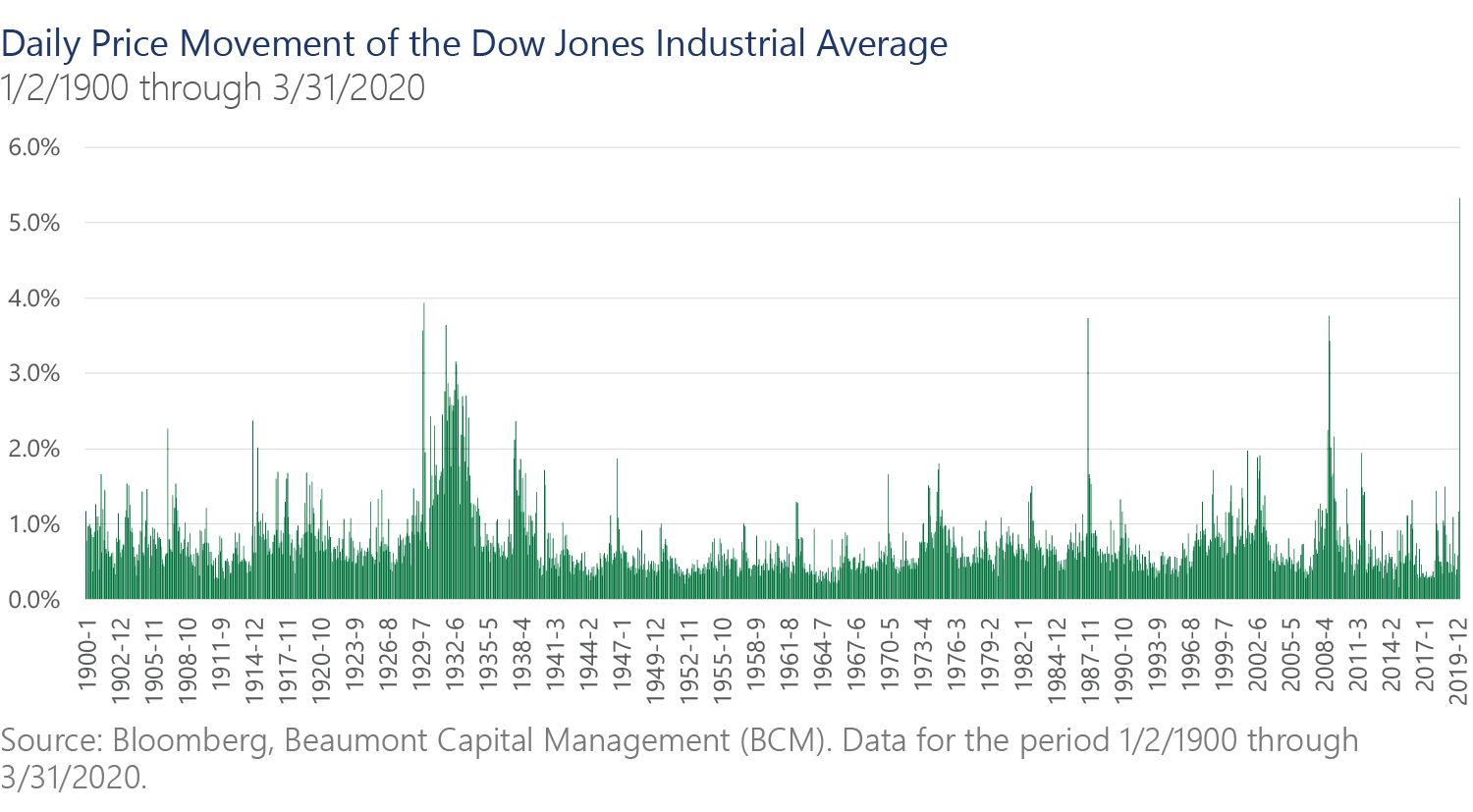

- The most 4%+ and indeed also the most 9%+ moves in the Dow Jones Industrial Average in any year since 1929

- A record high in the VIX (the CBOE volatility index)

- A massive oil market shock. The Saudi-Russian oil feud, a true “black swan,” changed the entire landscape of the oil market overnight. Over the course of the quarter, the price of oil fell nearly two-thirds including a decline of nearly 30% in a single day.

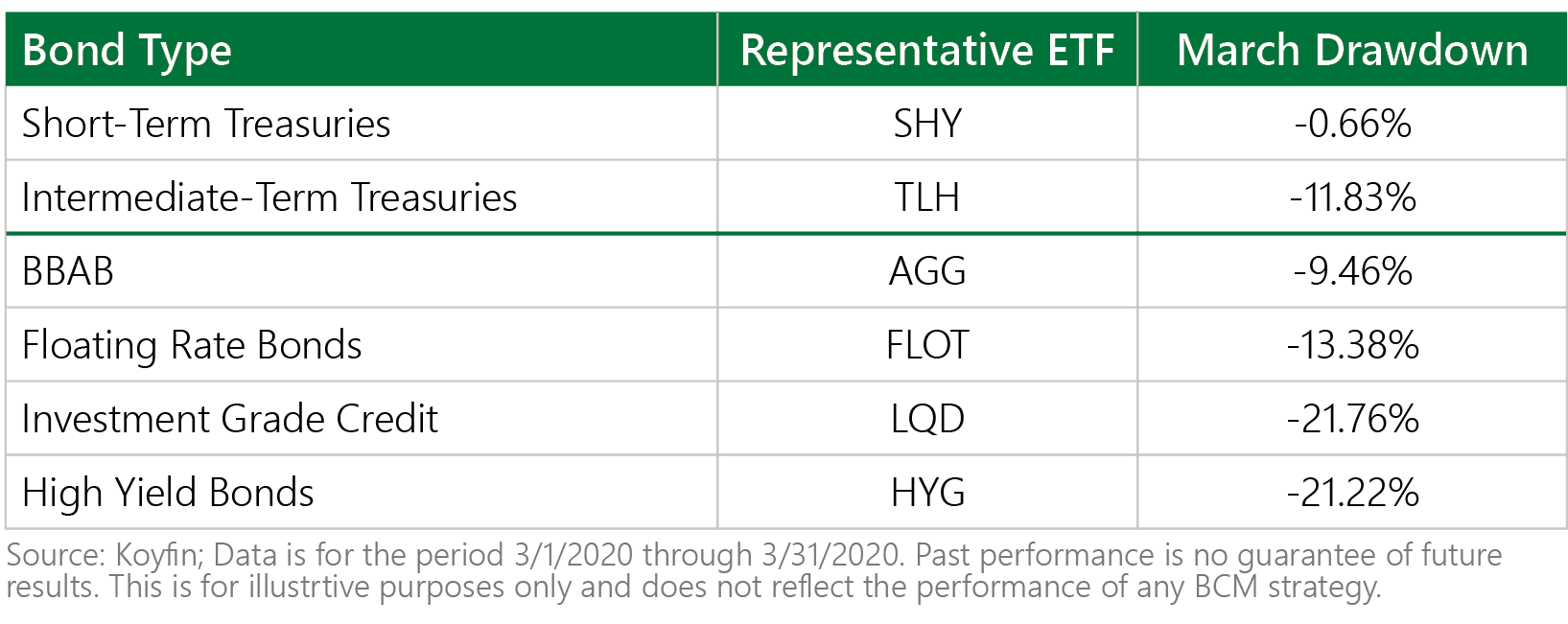

- Unparalleled volatility in the bond markets. Bonds, which entered the bear market with record low yields and credit spreads, offered less “protection” than any previous bear market. In fact, at the peak of the stock drawdown, bonds fell as well:

Suffice to say this bear market was unprecedented in terms of speed, explosiveness and breadth. The peak drawdown in the S&P 500® Index has been 33.9% so far, yet this may understate the general damage to investors as two of its largest sectors, Technology and Healthcare, substantially outperformed. Small-Caps, for example, incurred a significantly larger drawdown of over 42%, and now are barely positive on a trailing 5-year basis.

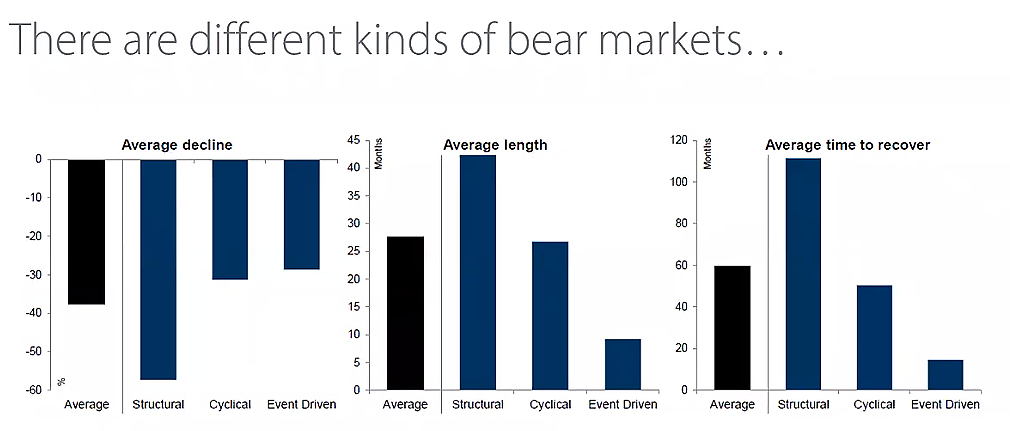

It is important to note that the end of the recent bull market and economic expansion was not caused by a misallocation of capital such as the excesses seen in 1999 and 2007. This is a self-induced, global economic shutdown necessitated by public safety. While it is impossible for anyone to know when and what is going to happen, with history as our pilot, this is likely going to take several quarters to several years to conclude. We first wrote about the Anatomy of a Bear Market several years ago and you can read the article here.

We believe that the duration of the pandemic will depend on what the “second-order” or spillover effects of this event are. It will also deeply depend on the diligence of people’s response (quarantine/social distancing) and whether government authorities rush to lift such preventative measures. If the flu pandemic of 1918-21 is a guide, there will be more than one wave of this pandemic before a vaccine is found and globally distributed. For example, most new cases in China are now being brought into their country from abroad. Covid-19 is so contagious, and so many victims are asymptomatic, that flare-ups across the globe and the resulting future quarantines will likely delay full economic recovery for some time.

The effects on our lives, our economy and our way of life are still being realized. We have seen airline traffic plummet 94%1, regional manufacturing fell up to 70%2, and millions of newly unemployed or furloughed workers. Corporate America borrowed almost $200 billion more in March alone3, much of this against their credit facilities. The scale of the disruption by itself is unnerving and as more data pours in, the specter of a quick economic recovery fades by the day.

The economy, especially the U.S. consumer, was very healthy going into 2020. If the economy can be “kept alive” with some of the supportive measures we discuss below, we could have a reasonably quick recovery as we are perhaps beginning to see in Asia. However, should this shock cause systemic damage, we may be looking at a traditional “business cycle reset,” akin to a cyclical or structural bear market, which is often a significantly more painful experience for investors.

Source: Goldman Sachs, Eventide Asset Management; as of 3/12/2020.

On the positive side, this hasn’t been a traditional financial crisis. With no misallocation of capital as mentioned above, essentially no one is to blame. We believe this has played a major role in how quickly both governments and central banks around the world have been able to act. The U.S. Federal Reserve has taken quick and decisive actions as they:

- Cut interest rates twice to “near zero” intra-meeting

- Bought ~$1 trillion of U.S. Treasuries and mortgage backed securities

- Backstopped the repurchase (repo) market with as much as $1.5 trillion4

- Re-opened the discount window to banks as an additional source of capital for loans5

- Re-opened the Commercial Paper Funding Facility to lend directly to U.S. business when the need arises6

- Opened swap lines of credit to 14 central banks across the globe to provide near-zero rates to those in need of dollars overseas7

Thus far, we have seen the U.S. Government produce a stimulus bill of $2.2 trillion…about 10% of our pre-crisis GDP. This is almost twice what the stimulus package of 2009 provided. The U.S. is not alone…Fiscal and monetary stimulus has been enacted in China, Europe, Japan, U.K., Australia, Canada and many more countries. Will it be enough?

Our three investment systems all share the same philosophy and purpose, but they go about it in different ways. Each is designed to reduce drawdown and volatility, but they were all trained on the past. The speed of recent events challenged the norm…all past bear markets, including 1987, took months or years to unfold…yet this one took weeks. While we are generally pleased with our performance, it is always wise to learn and adapt from recent events. Volatility always unearths opportunities for improvement, and we will continue to improve our processes and models to the best of our ability.

We seek to be the best possible stewards of our clients’ capital, and we thank you for your continued support.

Sources and Disclosures: