U.S. Broad Money Supply Climbs and a Look at Equities After the Rate Cut

September 20, 2019 | FIRESIDE CHARTS

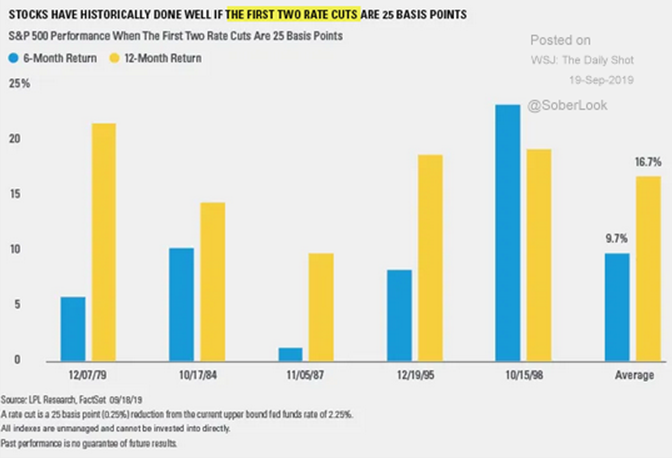

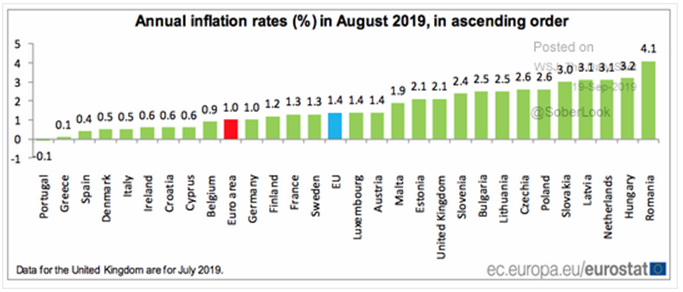

While the Fed’s second consecutive quarter-point rate cut this week disappointed many—including President Trump—who were hoping for more aggressive action, we’re encouraged by a look at how the S&P has historically performed in similar circumstances. An average 12-month return of 16.7% doesn’t sound too shabby! The market is now pricing in a ~65% chance of another cut by the end of 2019, but mounting dissent between committee members has complicated the picture. Meanwhile, despite bold policy action from the ECB, Eurozone inflation remains subdued with Portugal hovering in negative territory at -0.1%. Will their recent relaunch of QE be enough to kick-start lagging economic growth?

1. History tells us not to panic yet!

Source: LPL Research, as of 9/19/19

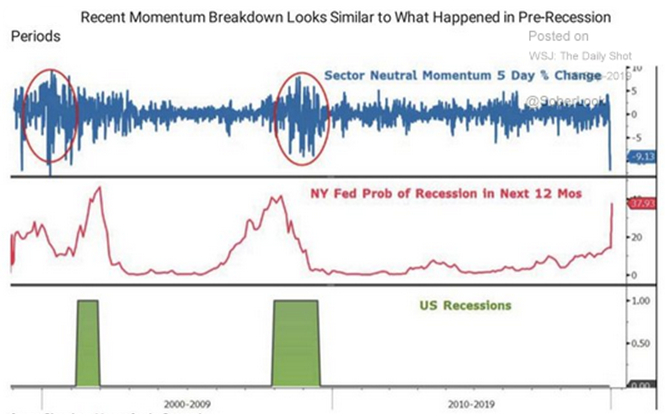

2. A lot of pessimism but little hard data to support an impending recession. The Fed gets an A+ for their part!

Source: Morgan Stanley Research, as of 9/19/19

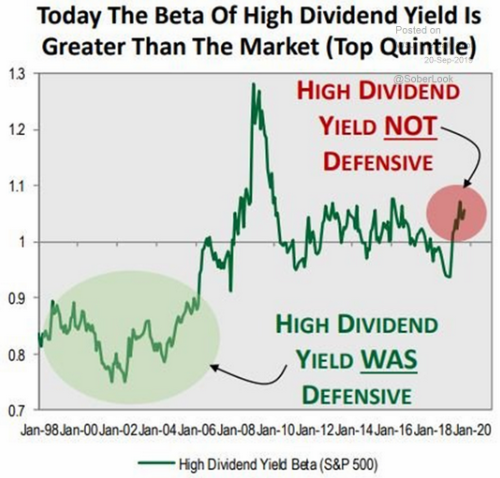

3. Have low interest rates made dividend stocks too expensive?

Source: WSJ Daily Shot, as of 9/19/19

4. Meanwhile, inflation remains stubbornly low in Europe despite the ECB’s efforts…

Source: Eurostat, as of 9/19/19

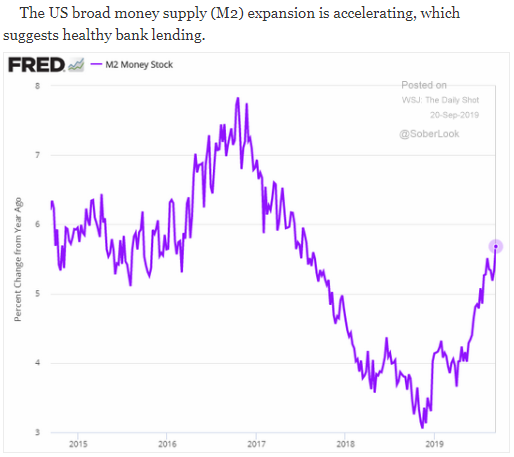

5. This is encouraging for the Financial sector and the economy as a whole…

Source: WSJ Daily Shot, as of 9/20/19

6. Still in expansion from last month, but the trend is still looking down…

Source: WSJ Daily Shot, as of 9/20/19

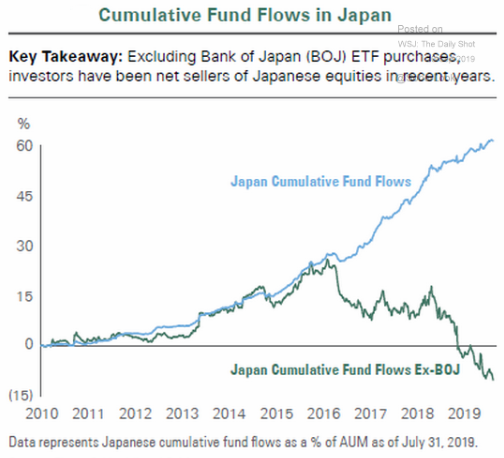

7. Is this going to end in a “disaster” for Japan? Can you imagine if 60% of the S&P 500’s purchases were by the Fed?

Source: Bessemer Trust, as of 9/20/19

8. We were asked a question on this yesterday…

Source: Bloomberg, as of 9/17/19

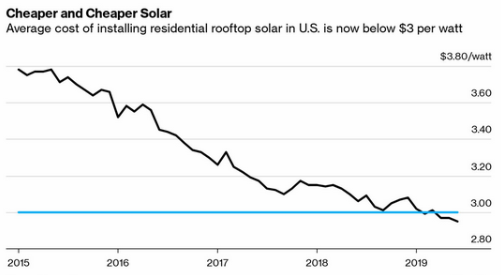

9. Ever consider solar for your home?

Source: Bloomberg, as of 9/19/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.