The GDP Hit, Unemployment, and a Look Ahead

May 1, 2020 | FIRESIDE CHARTS

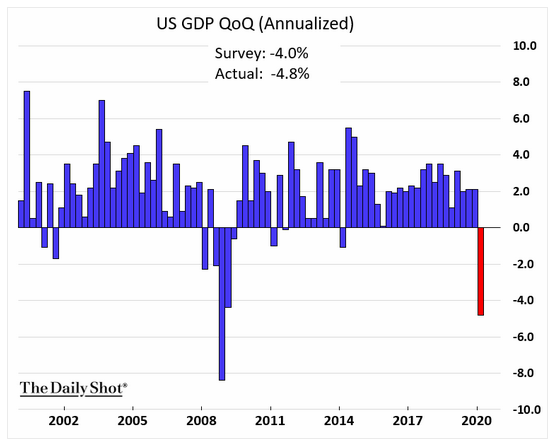

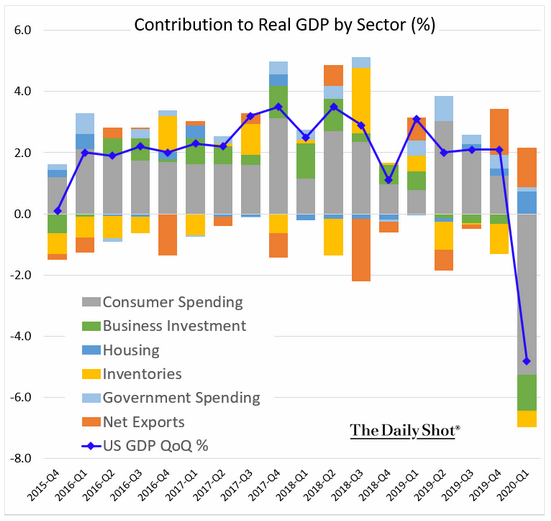

U.S. GDP fell at a 4.8% annual rate in Q1, posting its first quarterly drop in over half a decade and it’s worst quarterly drop since the financial crisis. Consumer spending, the main (re: ~70%) contributor to GDP, was the primary culprit after suffering its worst nosedive since 1980, and plunging business investment was the runner up. We’re already bracing ourselves for the Q2 print, with economists projecting a 30%+ annual decline. There’s been a lot of talk about Q3 as a turning point, but will the ghosts of infection risk and (perhaps more importantly) lost wages continue to haunt us long after the primary threat has lifted? Unemployment is at record highs and approaching 20% of the nation’s labor force, but how much of that population has seen their take-home pay jump thanks to the $600 boost to unemployment insurance? And did someone forget to tell the S&P 500® Index that there’s a pandemic going on? Despite the unprecedented blow to the economy, April saw the index clinch its best month since 1987—thank you tech stocks! But is it growing overextended? Meanwhile, debate continues about how, where, and when the economy should start to reopen, and what should change in the aftermath of the pandemic. With COVID-19 now the leading average daily cause of death in the U.S., opinions are plentiful. One thing’s for sure, we’ll be opting for head nods and elbow bumps over handshakes for the next few months…

1. If you only read one chart today, let it be this one. COVID-19 is now the leading daily average cause of death in the U.S.

Source: Flourish, as of 4/28/20

Source: WSJ Daily Shot, from 4/30/20

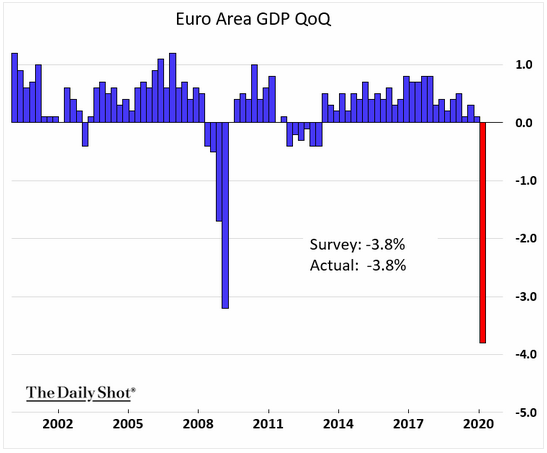

2. Since the COVID-19 lockdown didn’t start until part way through the quarter, we should set our expectations for a similar or even lower print in 2Q20.

Source: WSJ Daily Shot, from 4/30/20

3. The main driver was lower consumer spending. Even when lockdowns are lifted, many habits have changed and many consumers will be afraid to go out in public for some time…

Source: WSJ Daily Shot, from 4/30/20

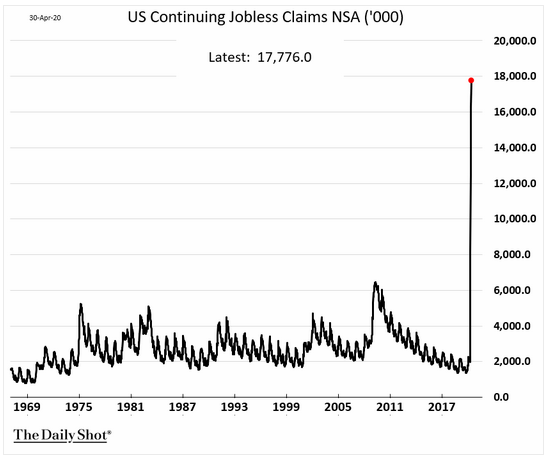

4. If we add yesterday’s 3.5 million new unemployment filings, continuing claims will likely top 20 million people.

Source: WSJ Daily Shot, from 5/1/20

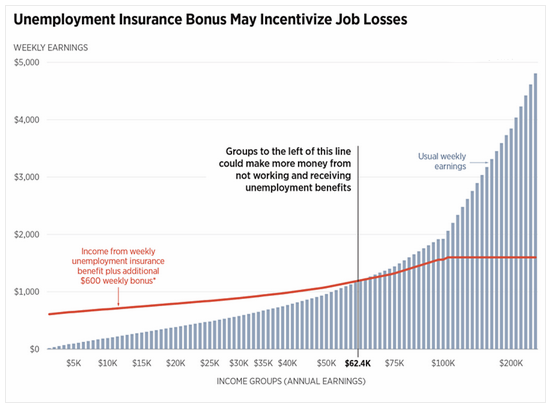

5. The Law of Unintended Consequence in action? We know of real situations where newly unemployed workers are not even trying to find work as they make more not working…

Source: The Heritage Foundation, from 4/29/20

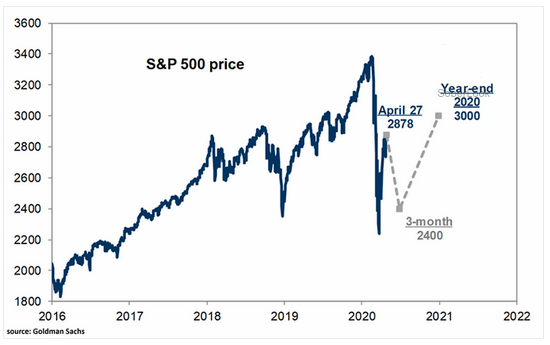

6. Many are warning that this rally is over-extended. Nothing is a foregone conclusion. Please keep your seatbelts fastened!

Source: WSJ Daily Shot, from 4/30/20

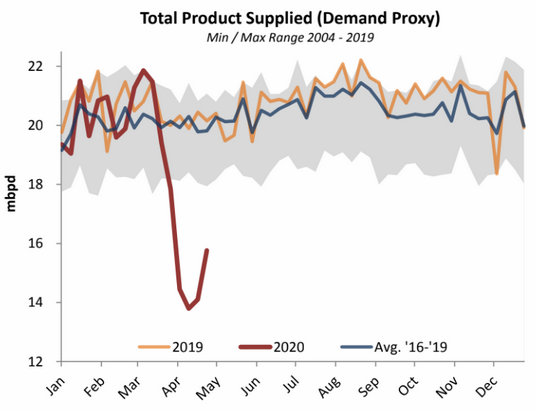

7. Energy is rallying around this print…U.S. gasoline demand has rebounded about 25% off the lows.

Source: Princeton Energy Advisors, from 4/30/20

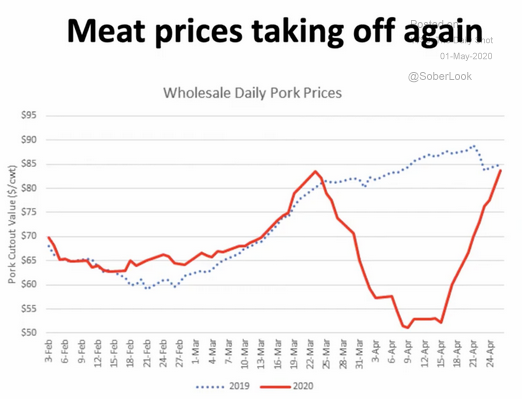

8. The COVID-19 increase, so far, has not pushed meat prices past where they were at this same point last year…

Source: Purdue University, from 4/28/20

9. Like the U.S., the virus hit part-way through the quarter. Depending on the speed of recovery, 2Q20 could be much worse.

Source: WSJ Daily Shot, from 5/1/20

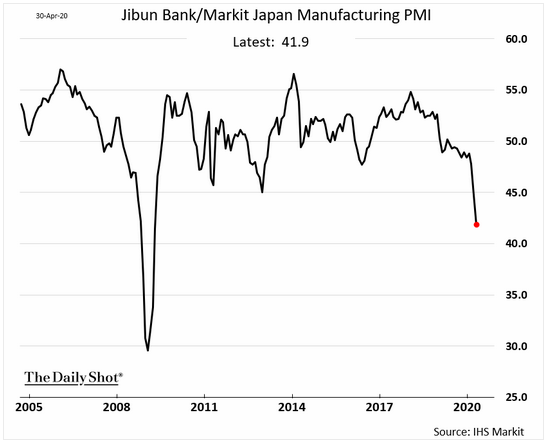

10. Japan has been holding up relatively well, but we note the Pandemic has yet to peak there…

Source: WSJ Daily Shot, from 5/1/20

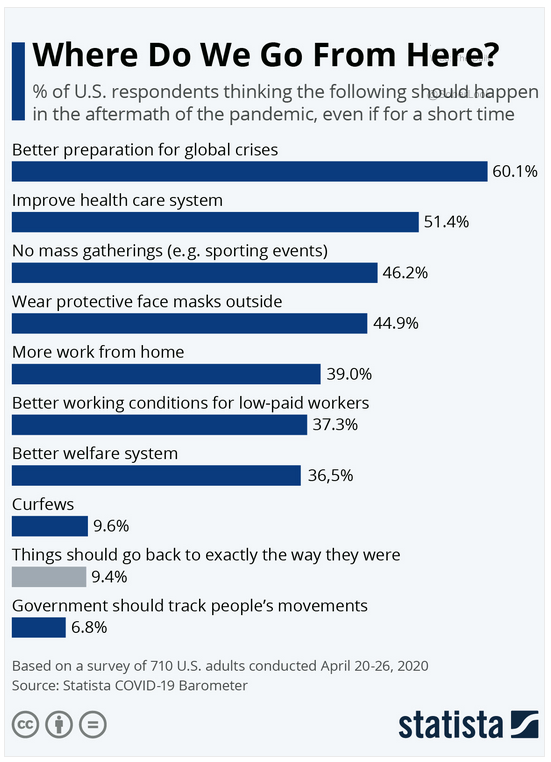

11. Will a broader consensus emerge after all 50 States have experienced their peaks? A good bet is that the numbers in Boston and New York are different…

Source: Statista, as of 4/26/20

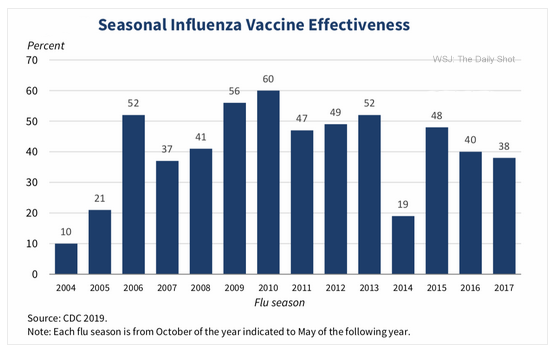

12. Will any future COVID-19 vaccine have similar effectiveness?

Source: The Council of Economic Advisors, from 9/15/19

13. Have you embraced the “elbow-bump” hello?

Source: Dilbert, from 4/20/20

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.