USD Hits 20-Year Highs, EM Currencies Set Record, and the Trade War’s Shock to Consumers

September 4, 2019 | FIRESIDE CHARTS

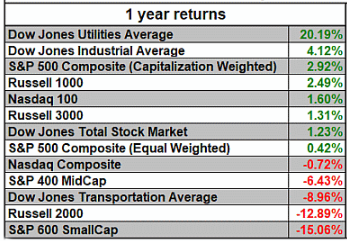

Let’s start with a quick August recap: the Dow Jones Utilities Average dominated last month with a 20.19% 1-year return, emerging market currencies—likely feeling the effects of the trade war and the USD’s record strength—suffered their worst August on record, and manufacturing woes continue across the globe. And the outlook for manufacturing and EM currencies may remain bleak, as the new round of 15% tariffs, now expanding into consumer goods, kicked in on Sunday. Should we expect consumer confidence, which has remained high throughout the summer, to take a dip?

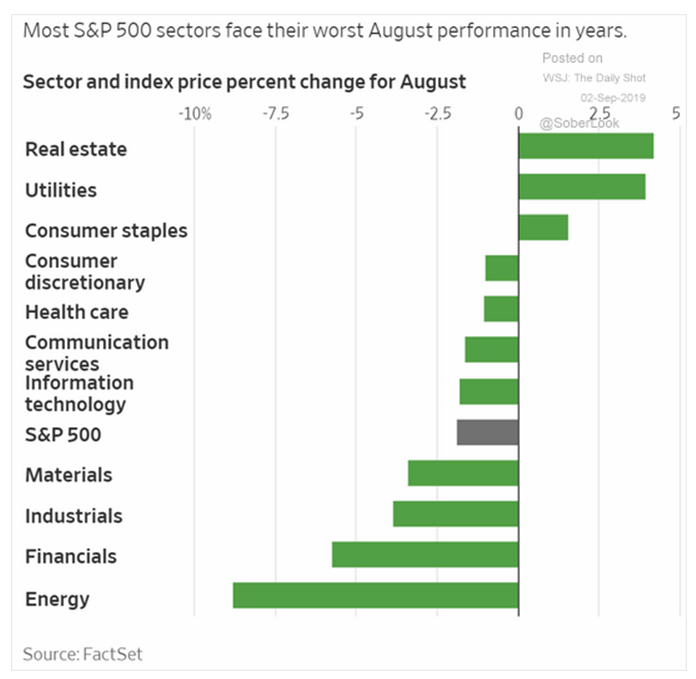

1. August was not kind to most sectors…

Source: FactSet, as of 9/3/19

2. We are willing to bet most would not have foreseen this…

Source: The Chart Store, as of 9/3/19

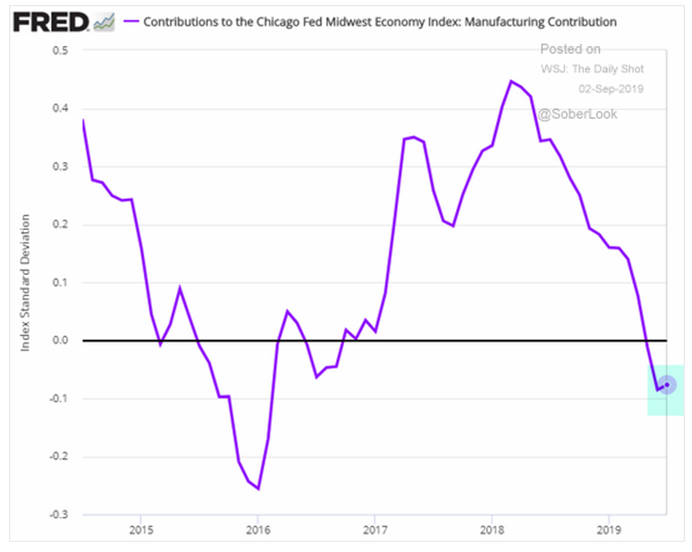

3. The Chicago Fed is still in negative territory, but any pause in the trend is welcome…

Source: FRED, as of 9/3/19

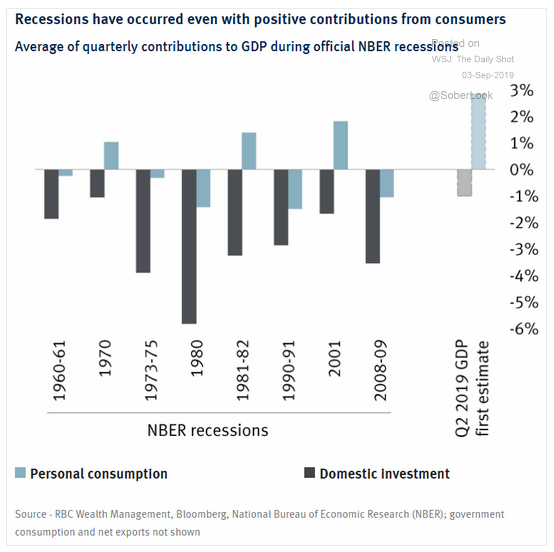

4. An interesting look-back at the U.S. consumer during recessions…

Source: WSJ Daily Shot, as of 9/3/19

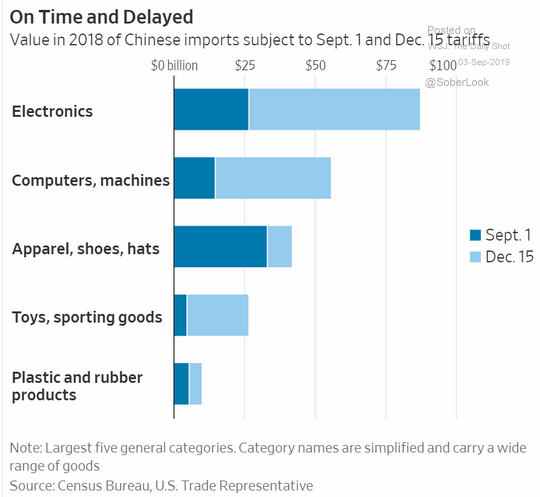

5. The U.S. consumer is going to get a shock as the previously announced tariffs go into effect. How will this affect the election?

Source: WSJ Daily Shot, as of 9/3/19

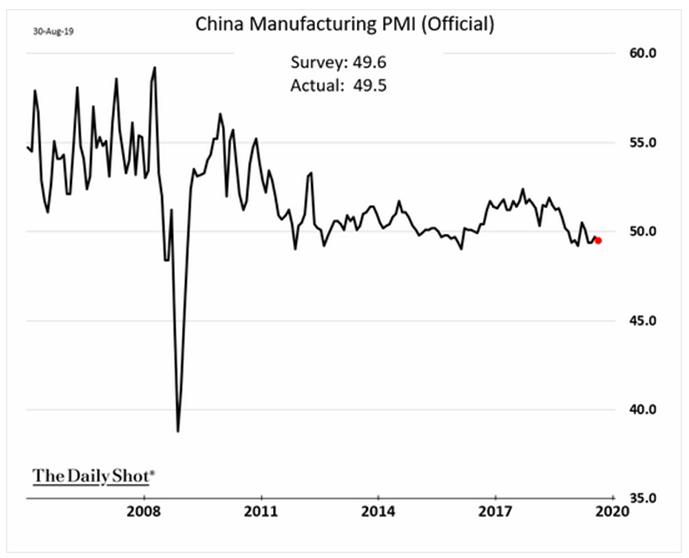

6. China’s manufacturing has been contracting for four months and the next round of tariffs kicked in this weekend…

Source: WSJ Daily Shot, as of 9/3/19

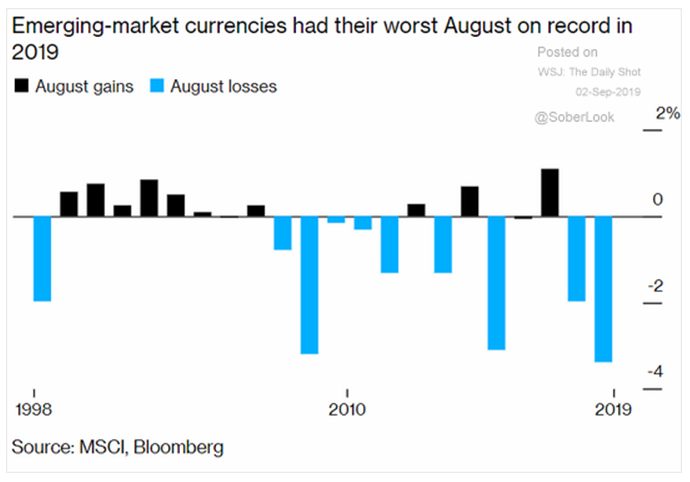

7. Collateral damage as China let’s “the market” devalue their currency?

Source: MSCI & Bloomberg, as of 9/3/19

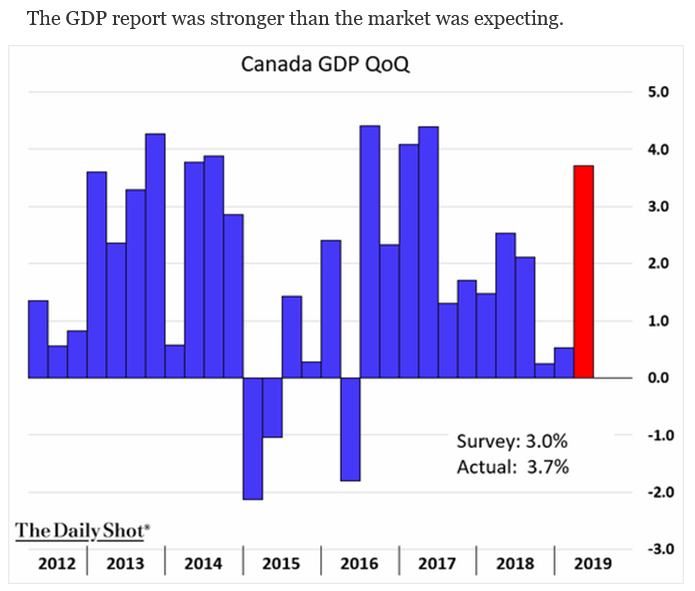

8. Unlike Mexico, Canada’s GDP had a great month.

Source: WSJ Daily Shot, as of 9/3/19

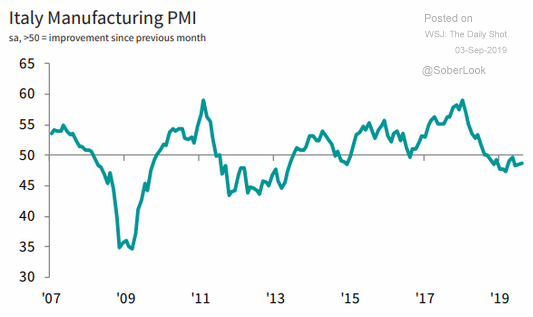

9. But Italy has joined Germany in manufacturing recession…

Source: WSJ Daily Shot, as of 9/3/19

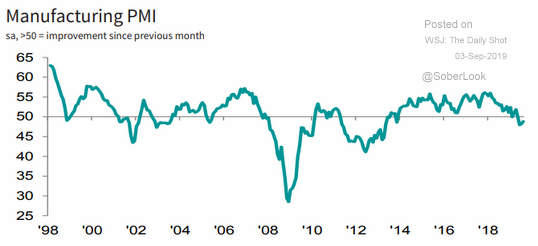

10. As has Spain…

Source: WSJ Daily Shot, as of 9/3/19

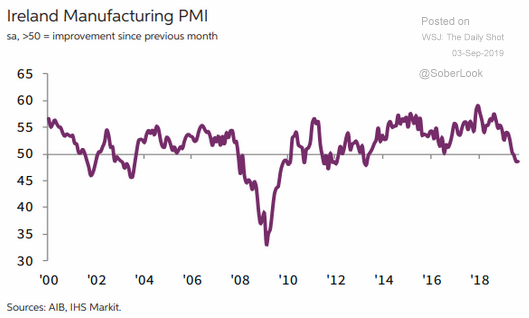

11. …and Ireland…

Source: WSJ Daily Shot, as of 9/3/19

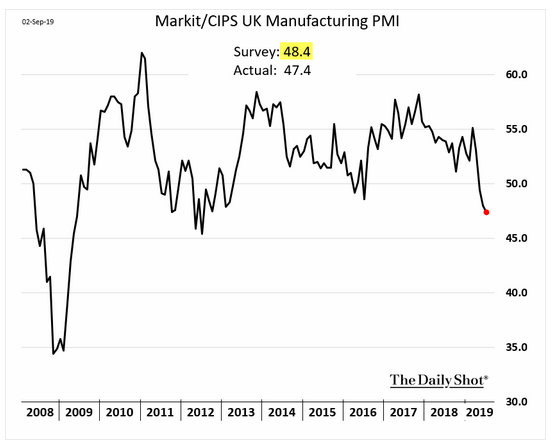

12. …and the U.K.

Source: WSJ Daily Shot, as of 9/3/19

13. As we mentioned last Monday, the U.S. is not immune and is also in a manufacturing recession. Moreover, the US dollar is now at 20-year highs which is making our goods and services more expensive overseas, a headwind for trade and Int’l sales.

Source: WSJ Daily Shot, as of 9/4/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.