1+ Years of Gains Erased, Jobless Claims Surge, Yield Curves Normalize

March 20, 2020 | FIRESIDE CHARTS

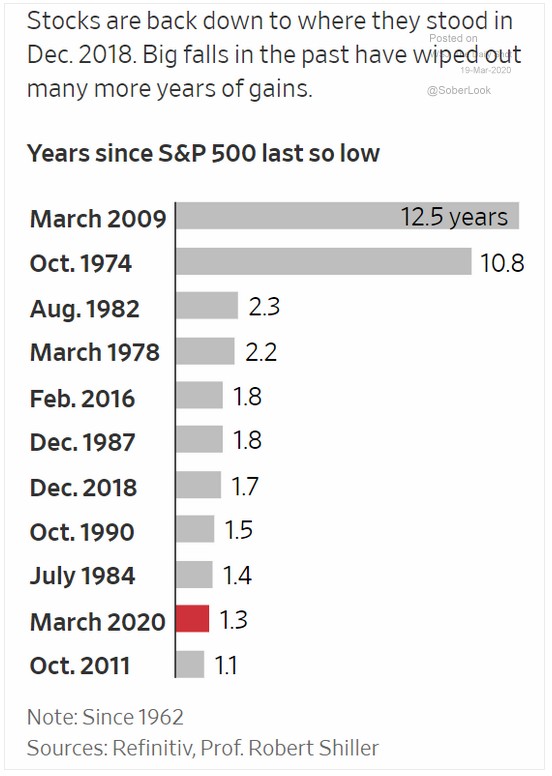

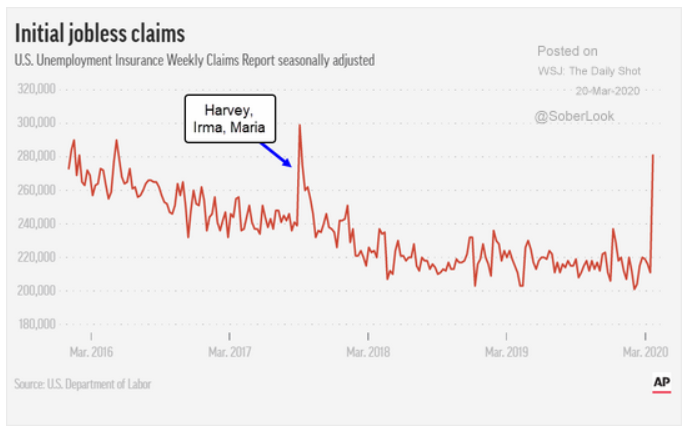

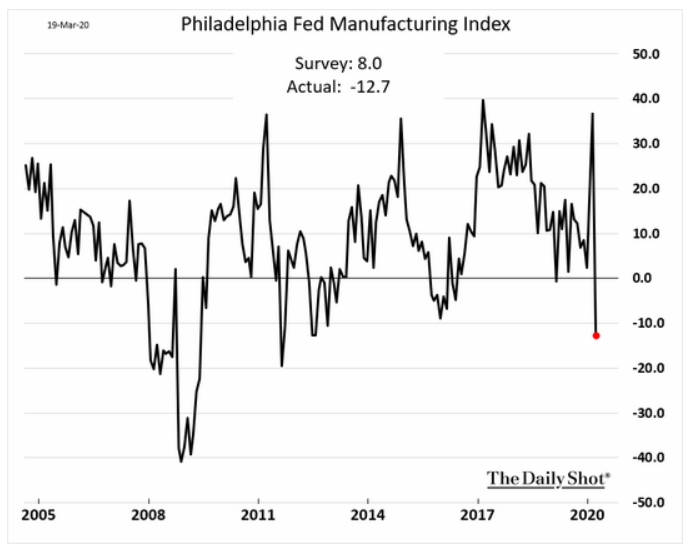

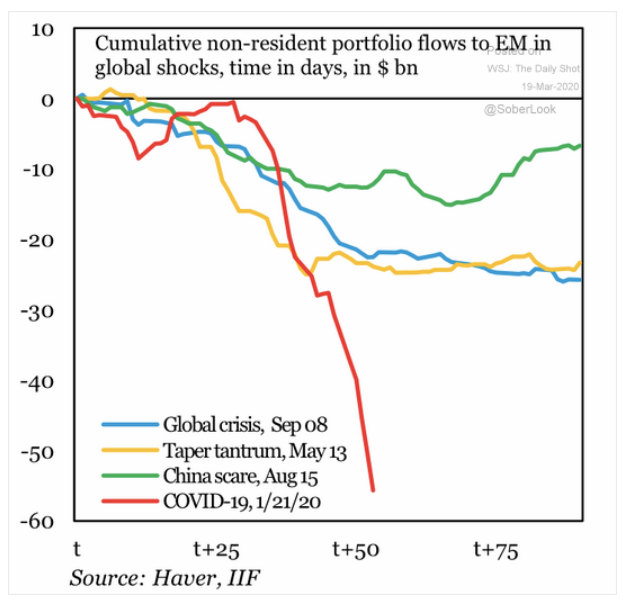

Stocks may have had a relatively stable day yesterday (by recent standards, anyway…) but a look back at history shows that we’ve so far only wiped out 1.3 years of gains, and—coming off the longest period of economic expansion on record—that means we have significantly more room to fall. Given the recent surge of unemployment claims—this week saw a jump of 70,000 and next week is projected to be worse—and the Fed’s recently adopted Sahm rule, it’s more than enough to signal an approaching recession. Are you prepared to ride it out? Unsurprisingly, manufacturing has plummeted, more than erasing its recent gains, and EM stocks have taken a significant hit. As the U.S. wades into the Saudi/Russian oil standoff and the Fed piles on additional stimulative measures, bond yields continue to wobble as investors struggle to make sense of the situation. Will additional global central bank intervention have the desired stabilizing effect? Let’s hope so, given the sky-high price tag. Finally, China’s recovery offers some hope that the situation may be relatively short lived. In the meantime, we’ll all be getting our money’s worth on housing costs as #socialdistancing continues and we settle into staying home as much as possible.

1. Based on history, the equity markets may have more room to fall…

Source: WSJ Daily Shot, from 3/19/20

2. The Sahm rule would predict immediate recession. The only questions are to the length and depth.

Source: WSJ Daily Shot, from 3/20/20

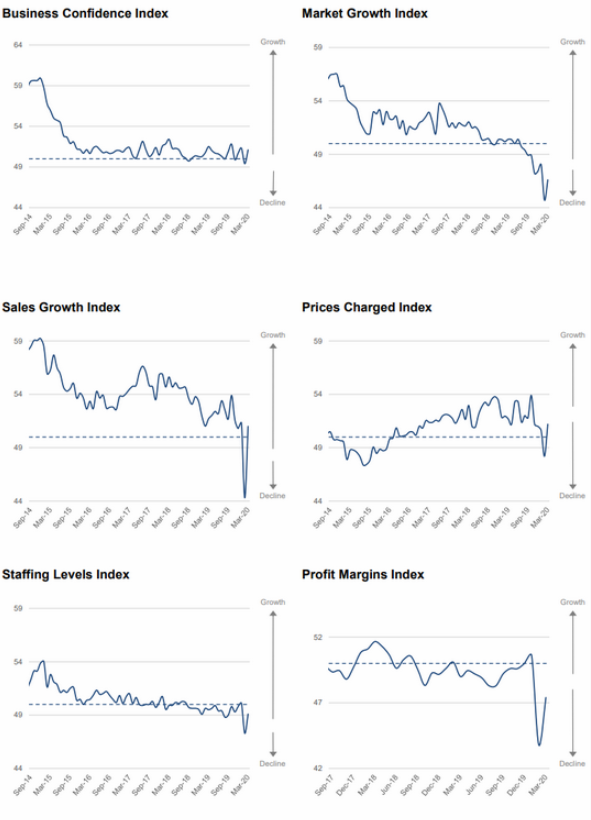

3. The Regional Fed surveys are also reporting what the markets have already started to price in, perhaps fully priced in for now…

Source: WSJ Daily Shot, from 3/20/20

4. EM investors are treating this as if it is twice as bad as 2008.

Source: WSJ Daily Shot, from 3/19/20

5. Don’t forget the other exogenous event… perhaps the Saudi/OPEC-Russian standoff will end soon…

Source: WSJ Daily Shot, from 3/20/20

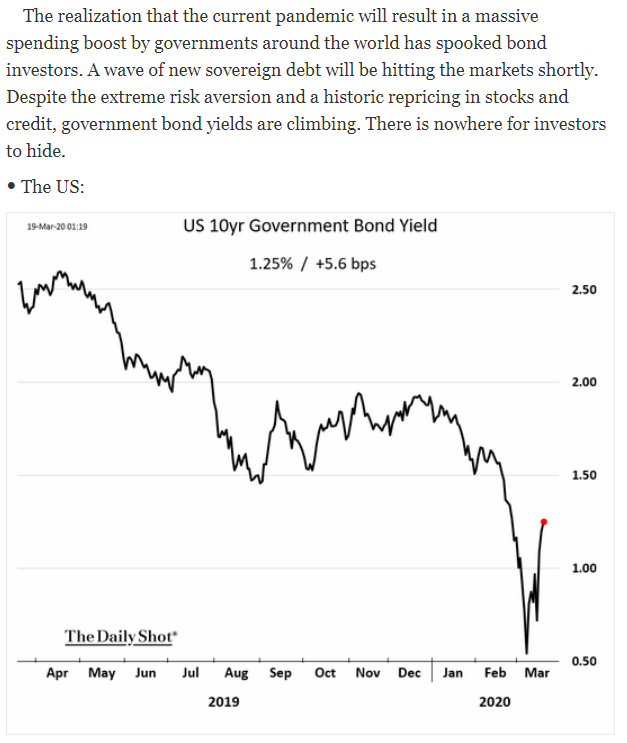

6. The pandemic has created a perfect storm of sorts. Yet the yield curve is normalizing in shape and the Fed is going to buy at least half the new UST’s….

Source: WSJ Daily Shot, from 3/19/20

7. Interest rates got so low that any reasonable yield curve normalization would cause large losses in fixed income. This is why all the QE is necessary to calm the bond markets…

Source: WSJ Daily Shot, from 3/20/20

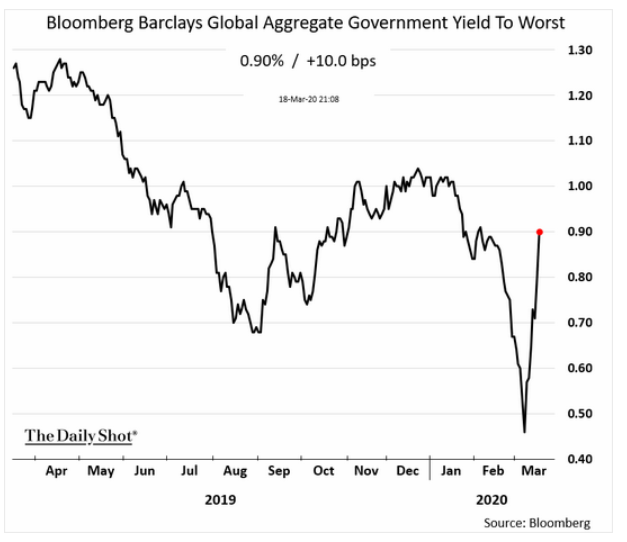

8. This is a global yield curve normalization… we are all in this together!

Source: WSJ Daily Shot, from 3/19/20

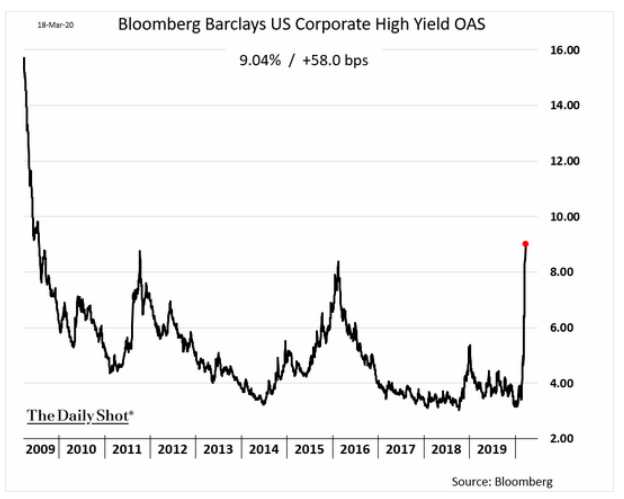

9. Junk bond yields are blowing out…

Source: WSJ Daily Shot, from 3/19/20

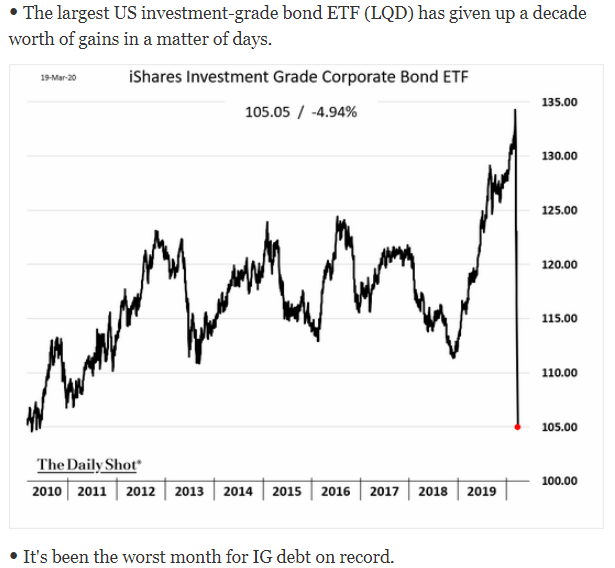

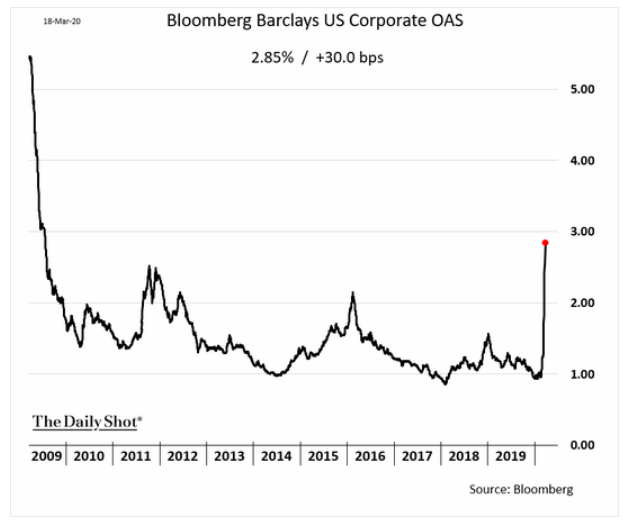

10. Even investment grade bond yields are rising substantively…

Source: WSJ Daily Shot, from 3/19/20

11. The Fed is going all out to help wherever needed. They seem determined to prevent any systemic breakdown…

Source: WSJ Daily Shot, from 3/19/20

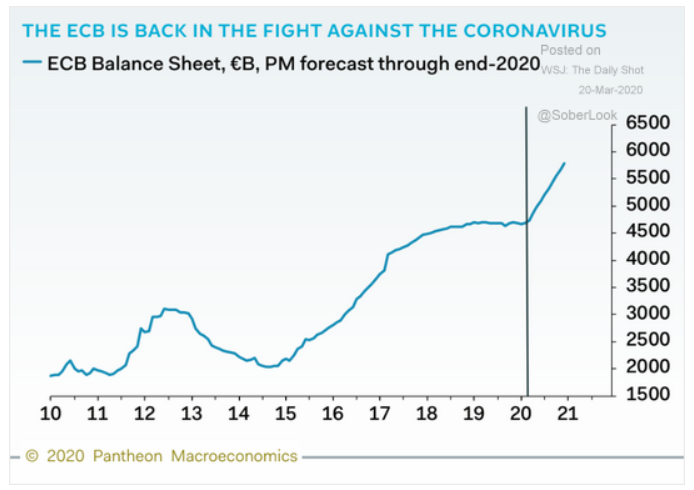

12. The Fed’s $500 billion, ECB’s 750 billion Euro and the BOE’s 200 billion pounds are just three examples of QE meant to stabilize bond markets and keep rates low across the curve…

Source: WSJ Daily Shot, from 3/20/20

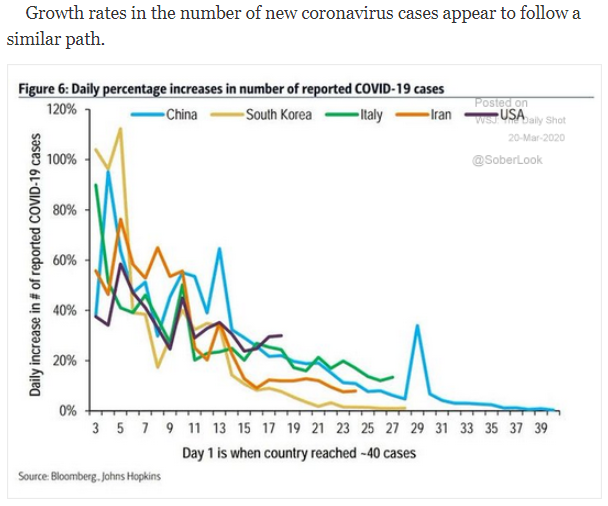

13. More and more data out of China suggests this is a 3-6 month phenomena as their economy has already started to recover…

Source: WSJ Daily Shot, from 3/20/20

14. We can defeat this! Who are you staying home for?

Source: WSJ Daily Shot, from 3/20/20

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.