U.S. Industrial Production Hits 2019 High, Inflation Measures Diverge

September 18, 2019 | FIRESIDE CHARTS

While we wait on Chairman Powell’s speech this afternoon, let’s take a look at what else is going on:

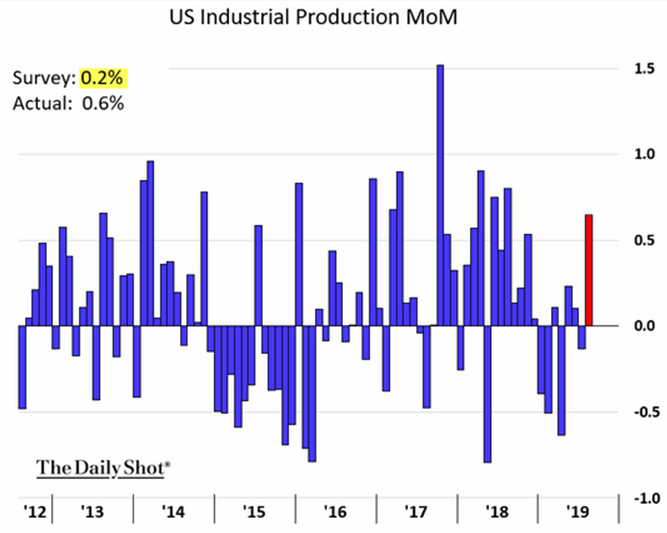

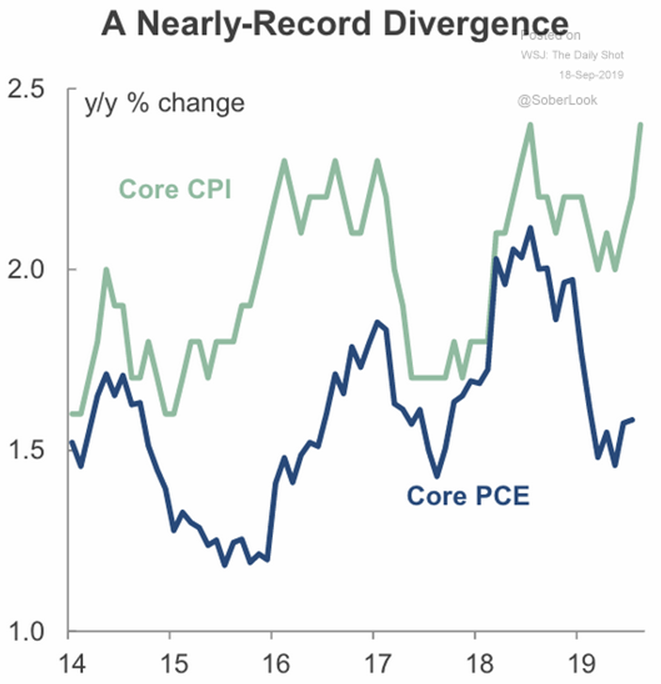

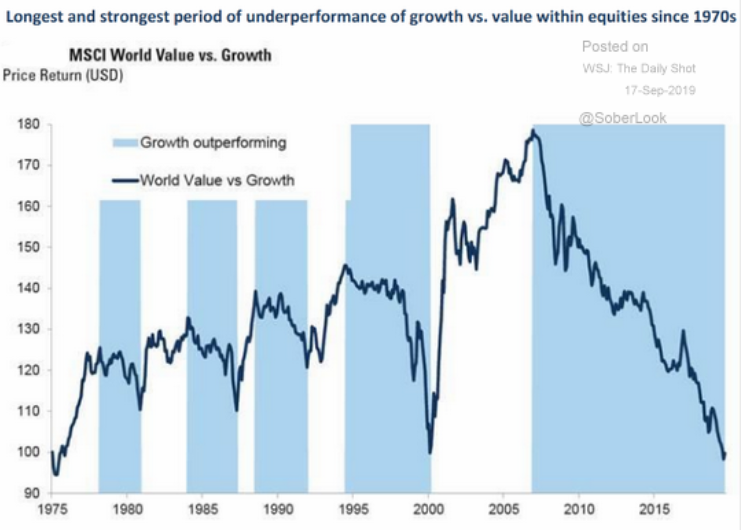

U.S. Industrial Production rebounded in August to reach a 2019 peak, approximately tripling the expected 0.2% print. Could this be a good sign of impending recovery for U.S. manufacturing? Turning an eye to consumers, the spread between core CPI and core PCE rose sharply in 2019, approaching all-time highs and complicating interpretations of inflation. While the Fed favors PCE, should we expect the nearly 1% higher CPI to factor into their decision today? Finally, MSCI growth is still dominating over value, and has been for over 10 years—more than double the length of any other period of out-performance since the 70’s. But how long can we expect it to continue as we’re already witnessing many investors begin flocking to safety assets like U.S. Treasuries?

1. Have we turned the corner?

Source: WSJ Daily Shot, as of 9/18/19

2. Does this make the Fed’s job a little trickier?

Source: Scotiabank Economics, as of 9/18/19

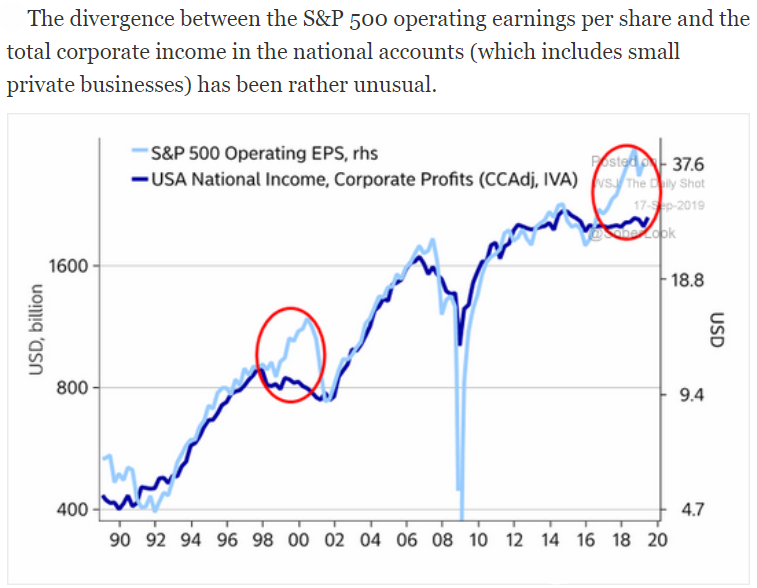

3. Are we in another 1999 scenario? This divergence may be implying so…

Source: Macrobond and Nordea, as of 9/17/19

4. All trends/cycles eventually come to an end…

Source: Goldman Sachs, as of 9/17/19

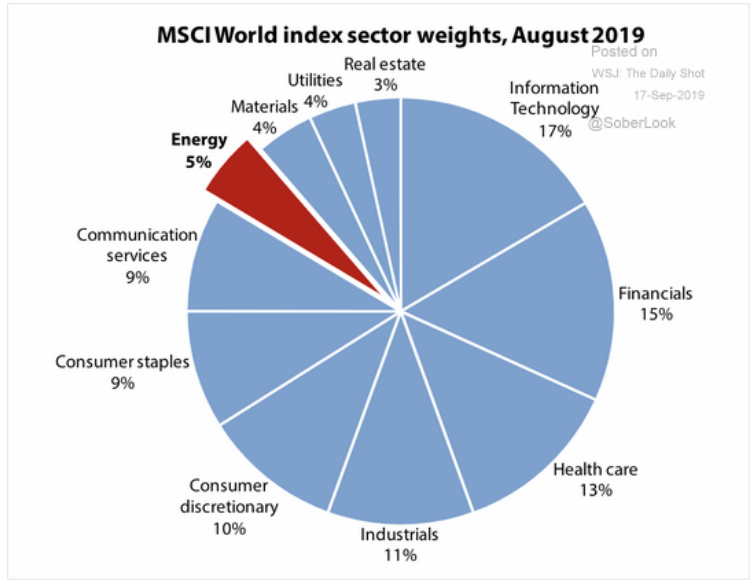

5. We caution against comparing market cap to economic importance…

Source: Gavekal, as of 9/17/19

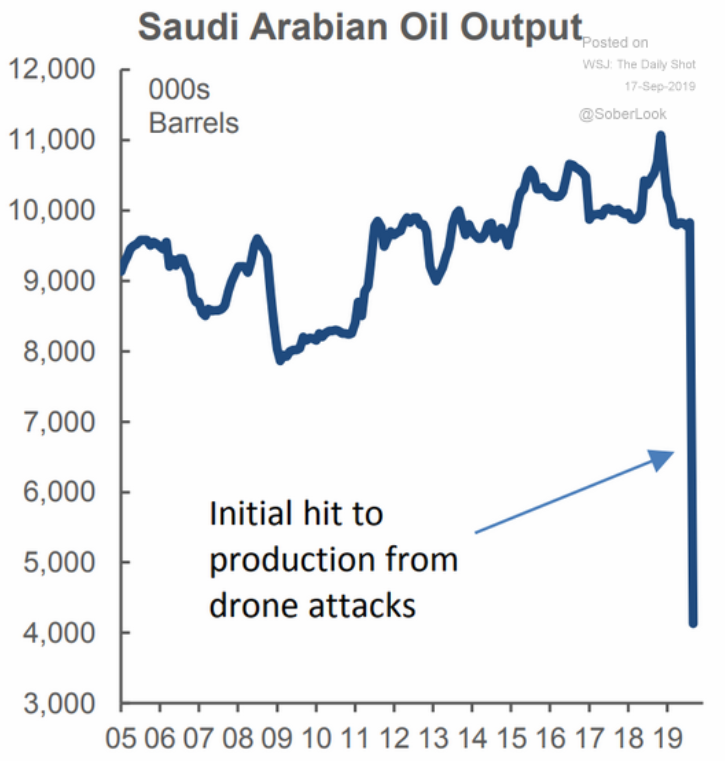

6. The attacks on Saudi Arabia’s oil infrastructure knocked ~5 million barrels a day off line. The issue is, for how long?

Source: Scotiabank Economics & Bloomberg, as of 9/17/19

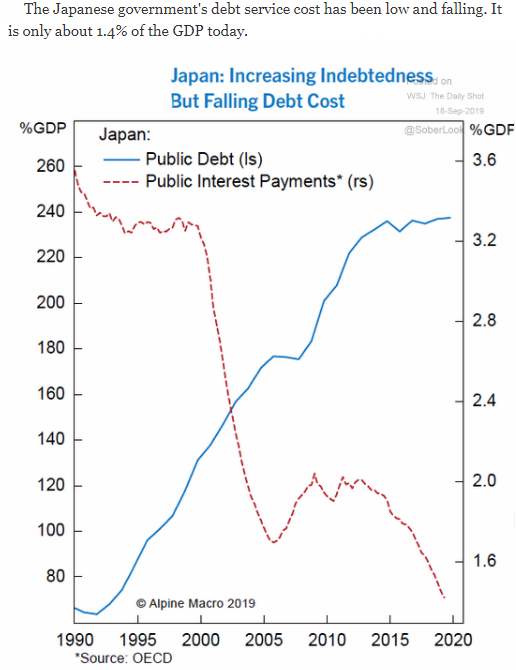

7. Negative rates have allowed Japan to borrow more yet pay less. Bar the door if inflation/higher rates ever materialize…

Source: Alpine Macro, as of 9/18/19

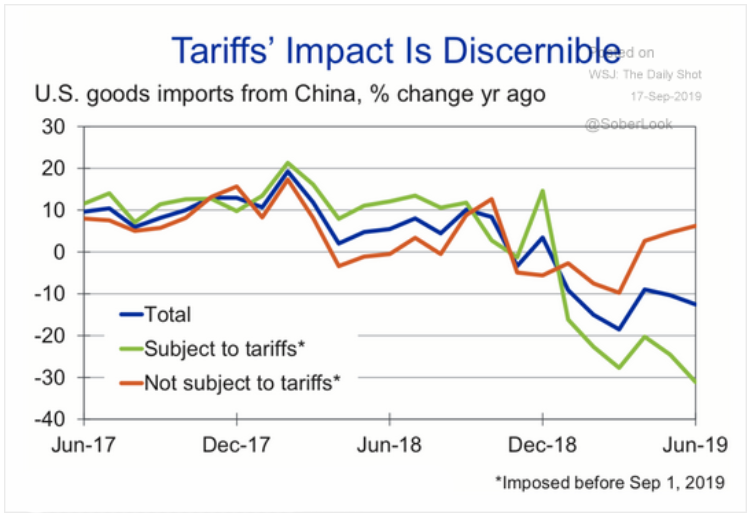

8. Both countries are “losing” the trade war…

Source: Moody’s Analytics, as of 9/17/19

9. Let’s take look back at the state of trade in 2018. Here we see the biggest importers…

Source: Howmuch.net, as of 8/27/19

10. …and the biggest exporters.

Source: Howmuch.net, as of 8/27/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.