Services Finally Feeling the Manufacturing Contraction, U.S. CEO Confidence Hits a Decade Low

October 4, 2019 | FIRESIDE CHARTS

While we digest today’s job’s report (50-year unemployment low, 136,000 jobs added, lower-than-expected wage growth—it’s a lot of data), take a look at some of the other major economic trends we’ve had our eyes on this week:

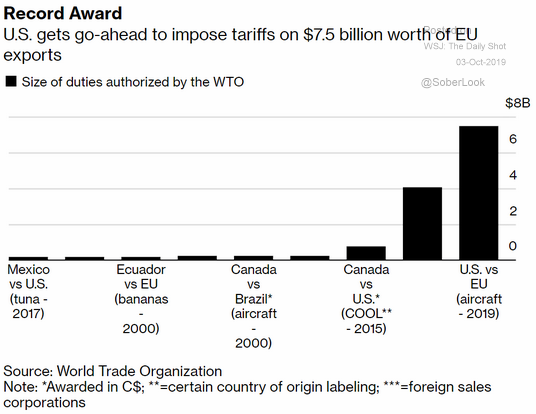

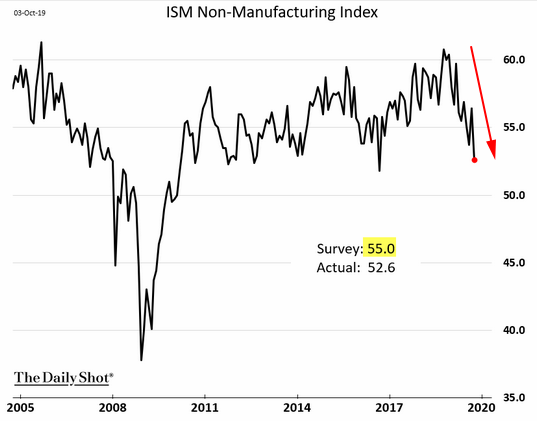

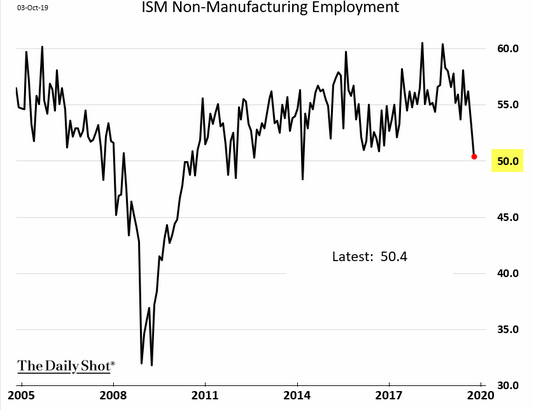

The trade war spread deeper into Europe this week as the WTO approved tariffs on $7.5 billion worth of EU exports on Wednesday. This comes in the same week that the organization slashed their forecast for global trade growth and attributed it almost entirely to the trade war—should we expect another revision lower when they meet again? And ISM data is still a hot topic this week as analysts turned their eye to the services sector yesterday: while manufacturing employment is firmly in contraction, non-manufacturing employment isn’t far behind at 50.4, and the non-manufacturing ISM index missed expectations at 52.6—a 3.8% MoM decrease and its lowest level since August 2016. Sorry folks, but it appears that the weakness in U.S. manufacturing that we’ve long been monitoring is finally bleeding into the broader economy… which we will discuss more in our quarterly commentary to be posted next week.

1. Here we go again… more tariffs on more countries. Europe is already a victim of the U.S.-China tariff trade war and now we open another direct assault?

Source: Bloomberg, as of 10/2/19

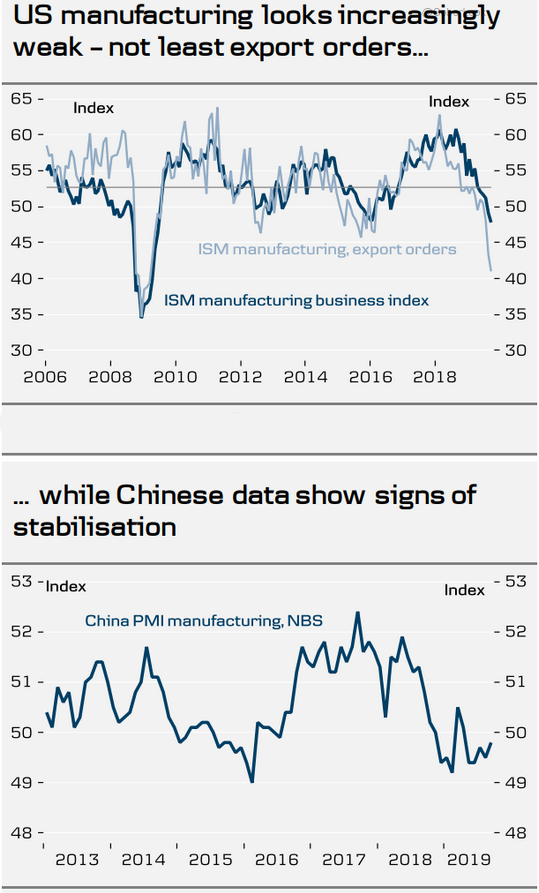

2. It appears the U.S. economy is getting the worst of the trade war…

Source: WSJ Daily Shot, as of 10/3/19

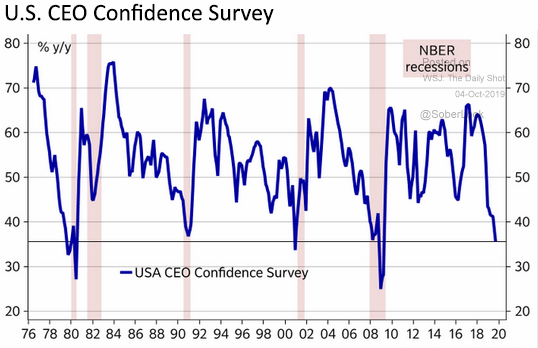

3. We have focused our concerns on manufacturing, but now the effects of the trade war appear to be affecting services and other areas of the economy. Will this trend continue?

Source: WSJ Daily Shot, as of 10/4/19

4. As we wrote in our quarterly letter—which will be posted to the blog next week—after a yield curve inversion, the coincidental indicator of a pending recession is an uptick in unemployment. The data from today’s job report will be crucial!

Source: WSJ Daily Shot, as of 10/4/19

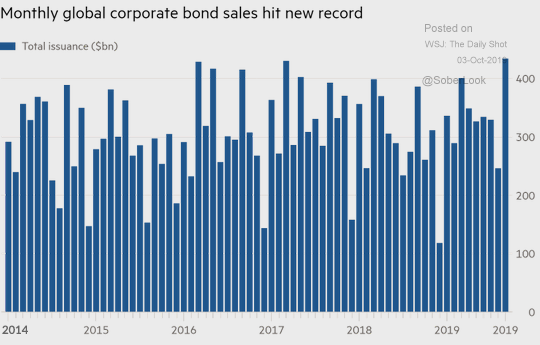

5. Another data point; should we start preparing for an inevitable recession?

Source: Macrobond and Nordea, as of 10/4/19

6. Given the low rate environment, this is not surprising…

Source: Financial Times, as of 9/30/19

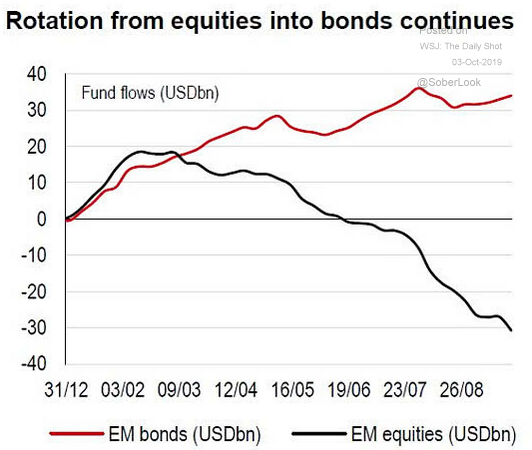

7. EM investors have been voting with their feet!

Source: IsabelNet, as of 10/1/19

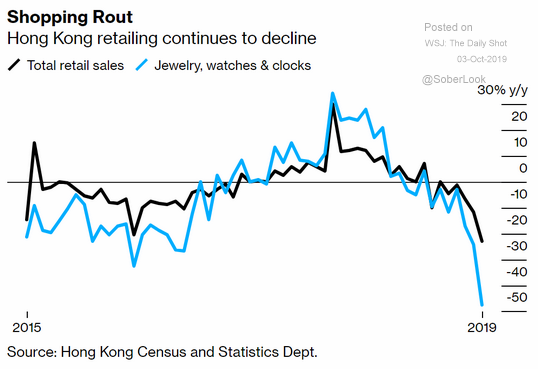

8. It is hard to go buy luxury goods when there is daily rioting in the streets…

Source: Bloomberg, as of 10/1/19

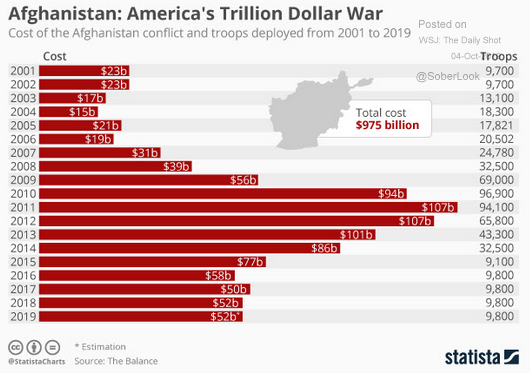

9. Was Charlie Wilson right? Imagine if half of this was spent on rebuilding infrastructure, schools, etc.

Source: Statista, as of 10/4/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.