Earnings Have Sparked a Rally; Is it Sustainable? And China Might be Winning the Trade War

October 16, 2019 | FIRESIDE CHARTS

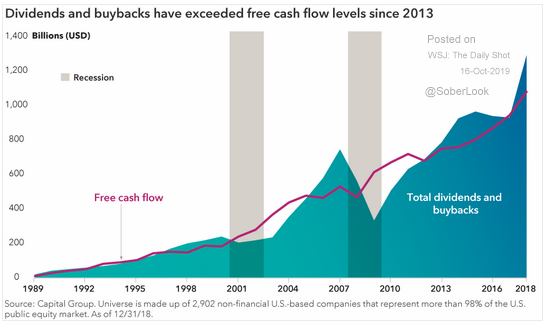

Earnings season kicked off in bullish style yesterday—with nine of the 11 reporting S&P companies either meeting or exceeding expectations—and sparked a market rally. While this eased many’s anxieties over market impact of the trade war, our optimism is more cautious as we remember how late-year estimates are often anchored low, and observe that much of the rally is attributable to only a few linchpin companies. Could that be thanks in part to the enduring trend of dividends and buybacks tying up (and exceeding!) cash flow? These companies may want to shore up some reserves, as the U.S. is losing market share—and potentially leverage at the negotiating table—to China, which is continuing to stall on solidifying last week’s “handshake agreement” in writing.

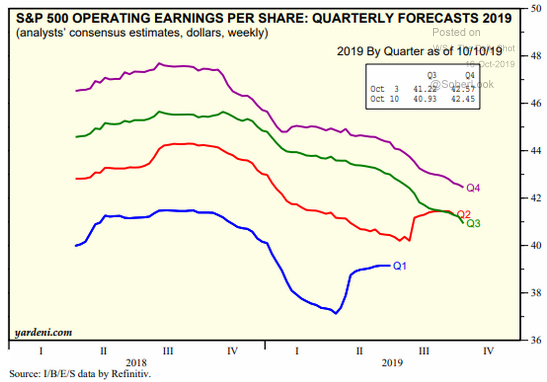

1. It is earnings season again! Will these trends continue?

Source: Yardeni Research, as of 10/10/19

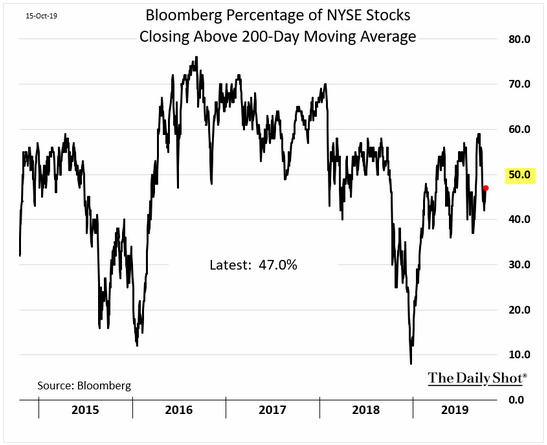

2. Once again, the current rally has been largely driven by the mega-caps. Less than half of the stocks on the NYSE are above their 200 day moving average…

Source: WSJ Daily Shot, as of 10/15/19

3. Will this excess come back to bite us in the form of over-leverage?

Source: Capital Group, as of 12/31/18

4. This makes sense as they are both are risk asset classes…

Source: WSJ Daily Shot, as of 10/15/19

5. The green is the U.S.

Source: WSJ Daily Shot, as of 10/15/19

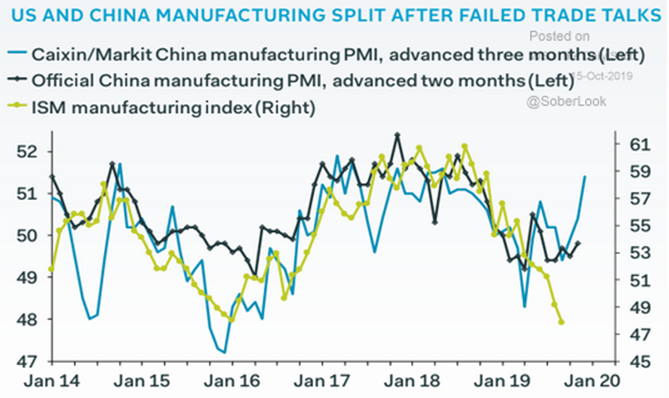

6. Between the PMIs and data like this, one can argue China has the upper hand…

Source: Oxford Economics/Haver Analytics, as of 10/15/19

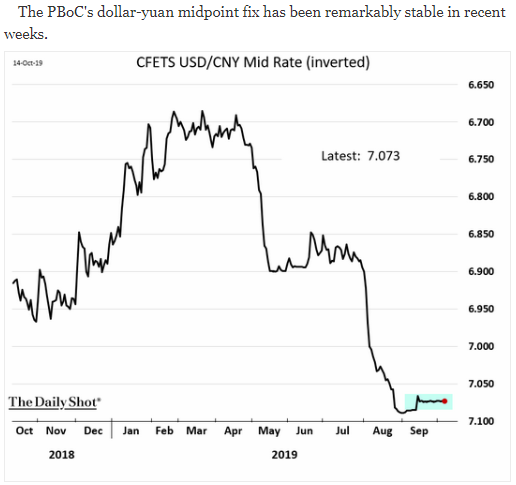

7. “Fix” being the operative word…

Source: WSJ Daily Shot, as of 10/15/19

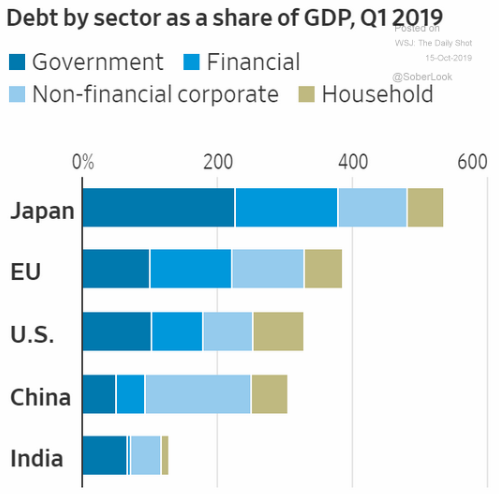

8. We wonder what is not counted such as unfunded pension liabilities…

Source: WSJ Daily Shot, as of 10/15/19

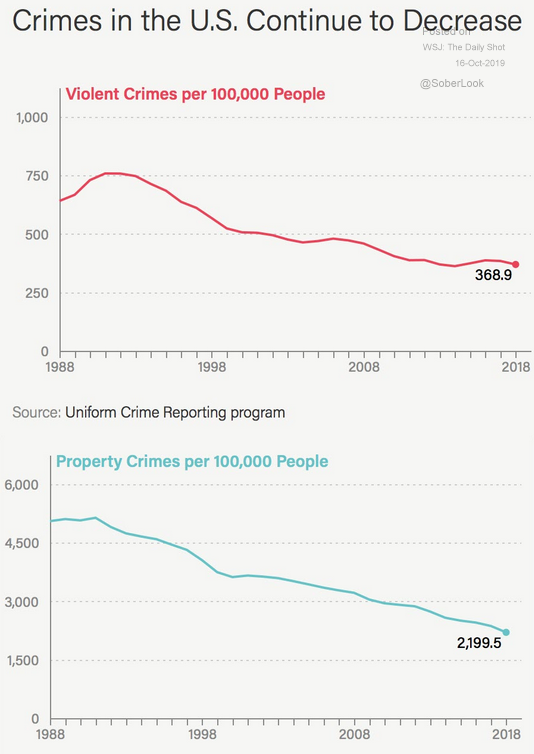

9. And some good news!

Source: The Marshall Project, as of 10/16/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.