Grim Forecasts, the Equity Rally, and Reignited Tensions with China

May 6, 2020 | FIRESIDE CHARTS

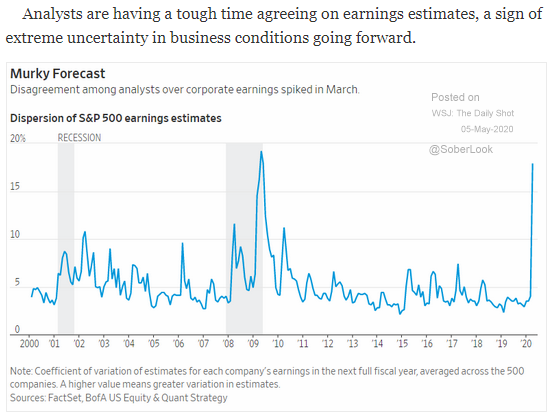

Halfway into an earnings season for the history books and analysts—much like the rest of the world—are still struggling to reach a consensus on what the future holds. The dispersion of estimates for S&P 500® Index companies has spiked to levels not seen since the financial crisis as our “new normal” has meant massive losses for some and gains for others. Looking forward through the rest of the year though, it’s clear they expect to see some level of contraction each quarter, with Q2 taking the hardest hit. And they don’t expect GDP to survive unscathed; current Q2 forecasts sit at -27.5%. Our economy has been devastated, but the memo doesn’t look to have reached the major equity indicies where the S&P 500 is down just 11.2% and the NASDAQ is down only 1.8%. Could a look at past bear markets give any hints about the current rally’s future? Meanwhile, the U.S. value factor just experienced its largest drawdown in history, TIPS yields have turned negative, and oil investors are scrambling to close June positions quickly after U.S. oil prices pivoted from massive April losses to enjoy a five-day winning streak. And as tensions ratchet up between the U.S. and China and the public grows more concerned about the conflict’s impact on their wallets, we’re turning our attention to how heavily we rely on China for essential medical supplies. Is now really the time to reignite the trade war?

1. Again, will disparate expectations move markets? The same report will both disappoint and exceed some analysts’ expectations. Will this cause volatility to remain elevated?

Source: WSJ Daily Shot, from 5/5/20

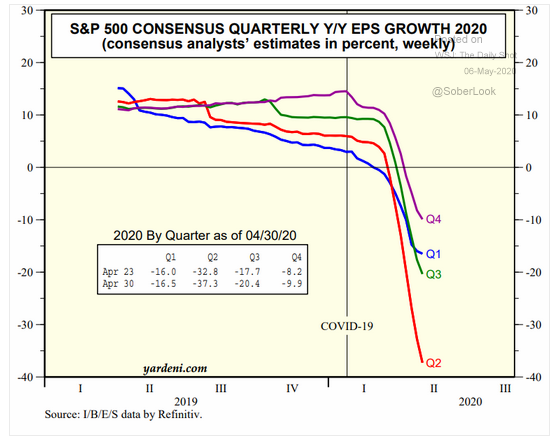

2. As the reality of a “V-shaped” economic recovery fades, earnings are being revised downward for future quarters as well…

Source: Yardeni Research, from 5/4/20

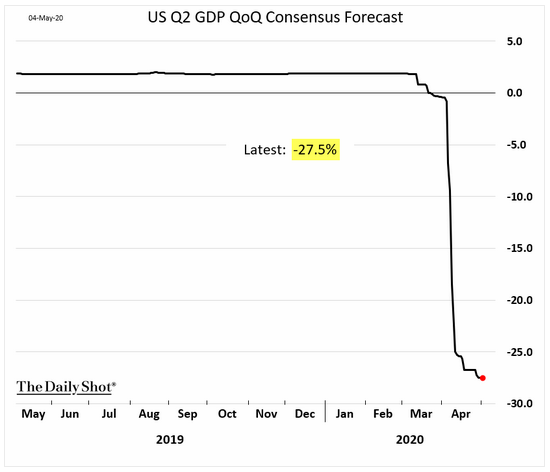

3. This is the consensus drop in U.S. GDP for the second quarter. How will the markets respond? It depends on investor expectations…

Source: WSJ Daily Shot, from 5/5/20

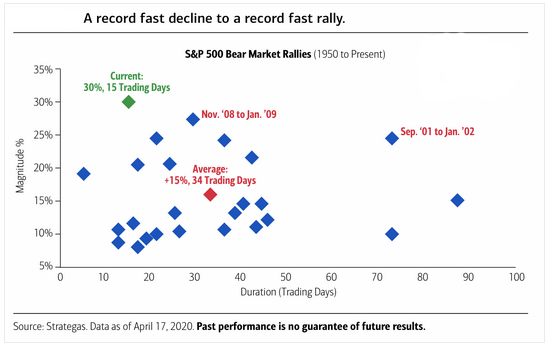

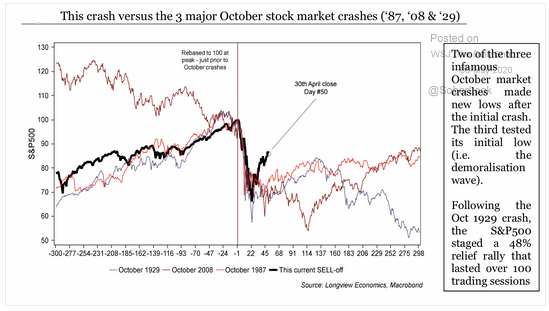

4. The speed of the recent bear market and the speed of the rally to date is unprecedented. Here is a comparison of the bears since 1950:

Source: bofA Merrill Lynch Global Research, from 5/5/20

5. Is this rally ahead of itself? No one knows, but discipline and flexibility certainly help!

Source: WSJ Daily Shot, from 5/6/20

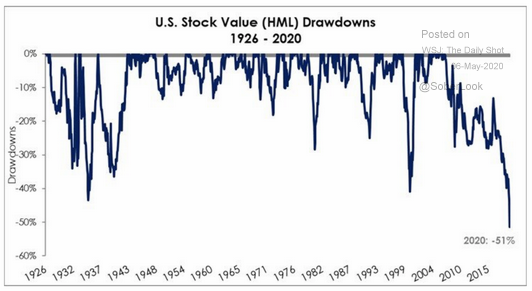

6. Another example of why “smart beta”, by itself, is not so smart…

Source: Two Centuries Investments, as of 3/31/20

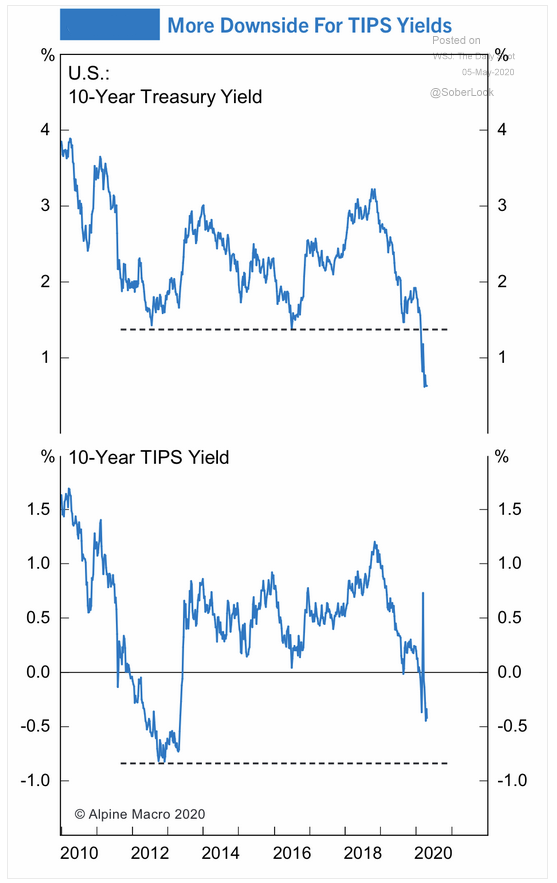

7. TIPS yields have turned negative. Will regular Treasuries follow suit?

Source: WSJ Daily Shot, from 5/5/20

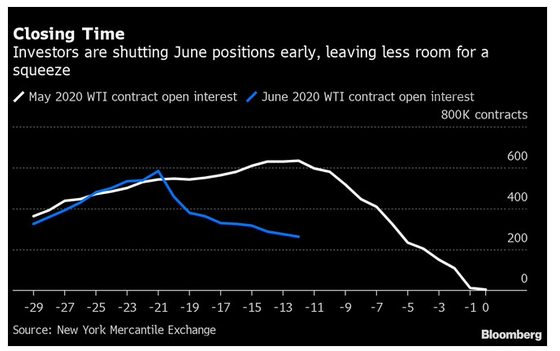

8. After the May contract went negative near the settlement date, investors are “once bitten, twice shy”…

Source: Bloomberg, from 5/4/20

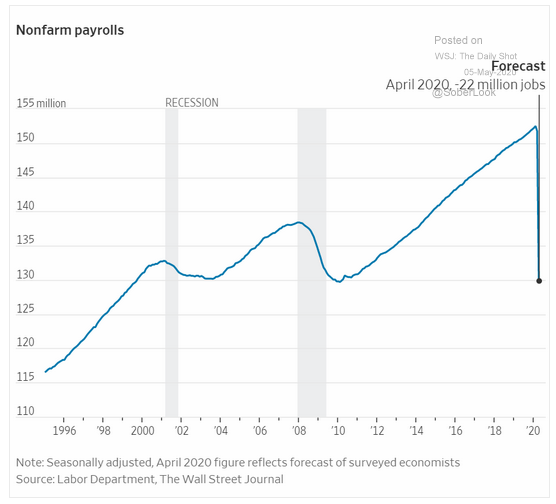

9. As businesses run out of cash, the unemployment picture deepens. It is now expected that the number of jobs lost exceeds the number of jobs created since the Great Recession.

Source: The Wall Street Journal, as of 5/3/20

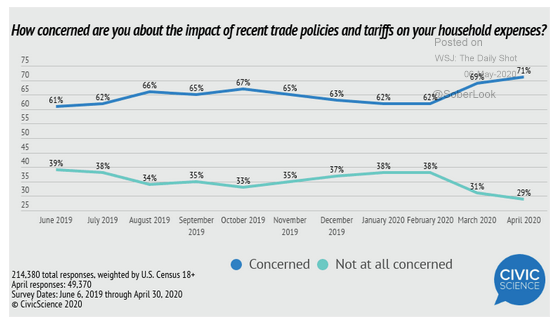

10. Given the magnitude of the pandemic, is it time to put trade and profit on hold for a few months?

Source: Civic Science, from 5/4/20

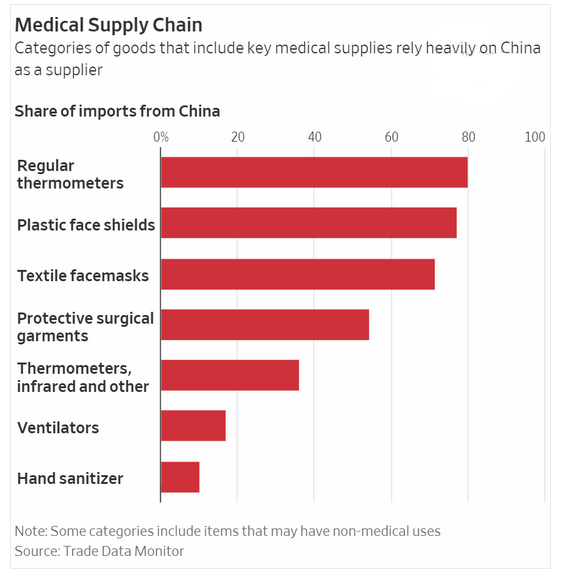

11. Since China needed these items themselves to combat the pandemic, what was left for us (U.S.)?

Source: WSJ Daily Shot, from 5/5/20

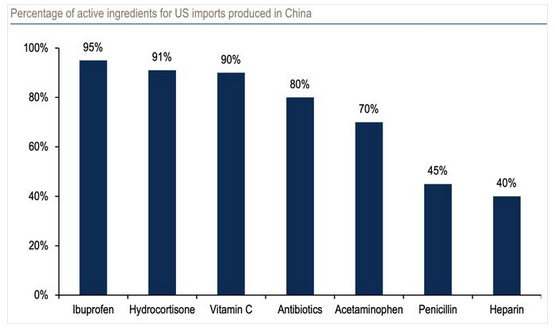

12. …The same goes for many drugs:

Source: BofA Merrill Lynch Global Research, from 5/5/20

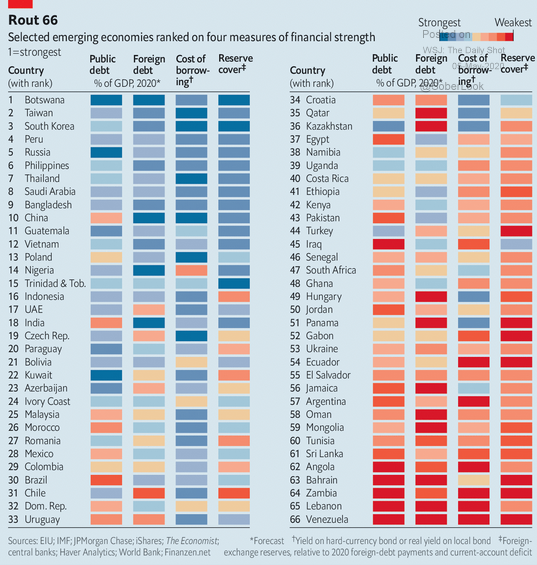

13. A great list of EM countries and their relative strengths and vulnerabilities:

Source: The Economist, from 5/2/20

14. Which sign off are you using these days?

Source: NewYorker.com, from 4/22/20

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.