Analyzing Friday’s Rally and Are Emerging Markets Preparing to Surge?

October 7, 2019 | FIRESIDE CHARTS

Happy Monday, Fireside Charts readers! We know Mondays can be a little rough (and you’ve got a lot of emails to get through), so we’ll stick with the highlights today:

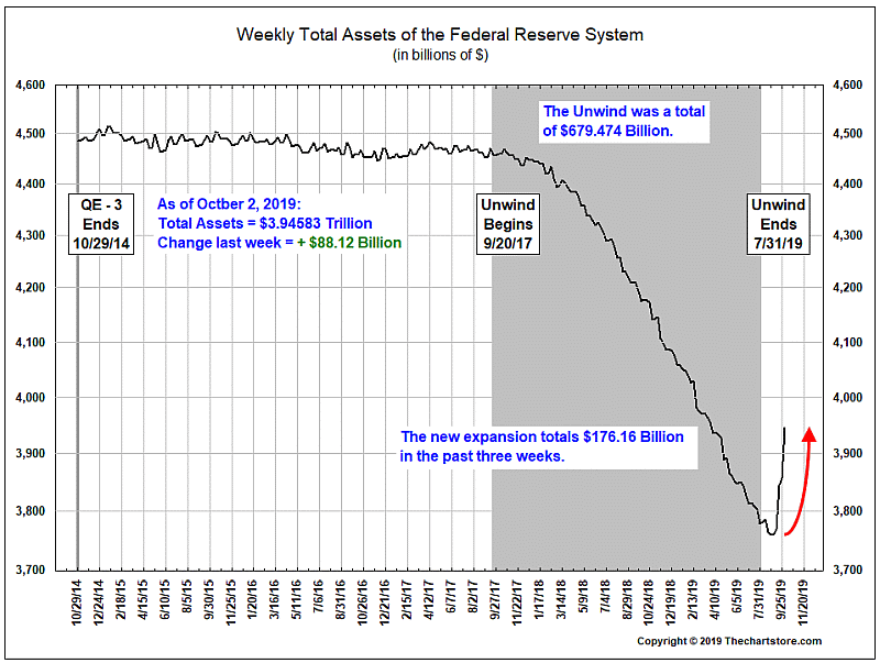

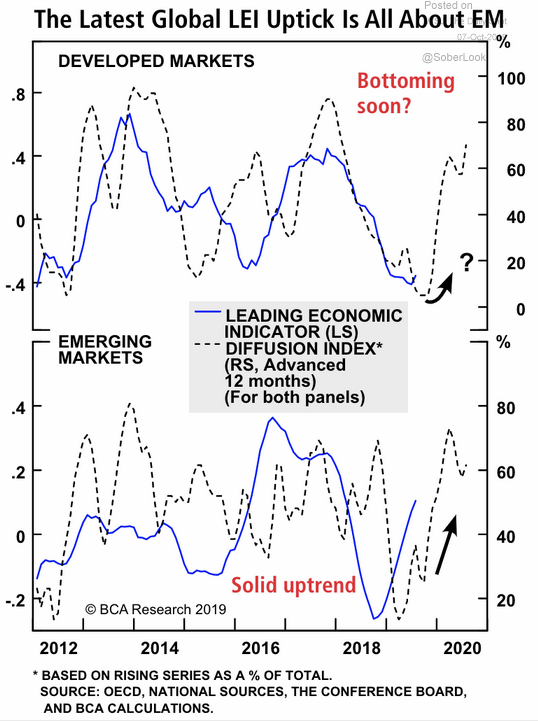

We saw a modest rally on the back of Friday’s better-than-feared jobs report, but it appears primarily driven by anticipation of additional rate cuts rather than a surge in economic confidence. Even the hawks don’t seem to be completely closed to further easing, as yesterday KC Fed President and known hawk Esther George conceded that “there are certainly risks to the outlook” and “adjusting policy may be appropriate” should more disappointing data come in. We say further easing, because as of Friday the Fed has already laid out $176 billion worth of QE in the last three weeks alone—could that be an indication of what to expect from the October meeting? Meanwhile, we’re keeping our eyes on emerging markets as EM equities have softened to match the broader market, but EM LEI’s are rising at a much faster clip than their developed market counterparts. Could the sphere be poised for revitalization?

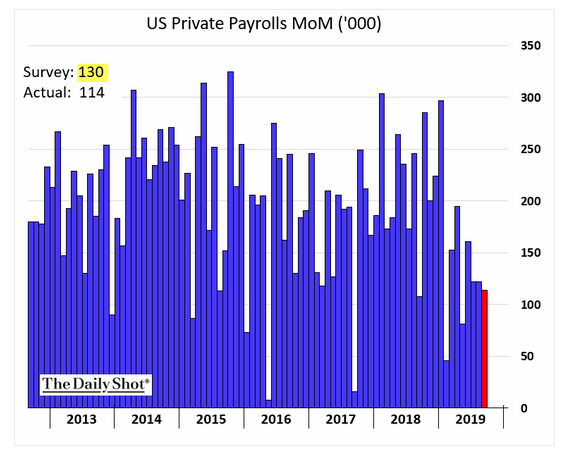

1. The market surged on Friday after the payroll report. It turns out the jobs report was less than expected, but August was revised up. The surge is more based on the market thinking the Fed will cut two more times this year…

Source: WSJ Daily Shot, as of 10/7/19

2. Few are talking about it, but the Fed has quietly re-started QE!

Source: The Chart Store, as of 10/4/19

3. Perhaps this is why the FAANG stocks have been struggling of late…

Source: Axios Research, as of 9/17/19

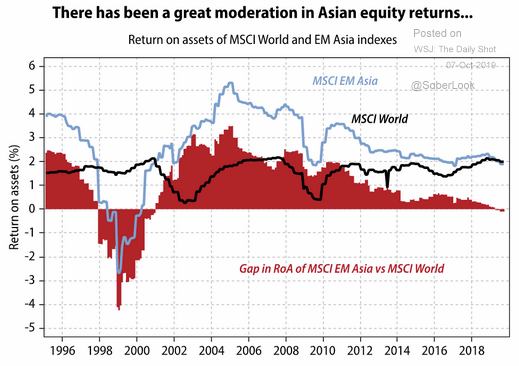

4. No trend lasts forever… Will EM equity return to its heyday in 2020?

Source: Gavekal, as of 10/7/19

5. The economic data is beginning to support an EM resurgence…

Source: Longview Economics, as of 10/7/19

6. And umm… here’s a look at which filler words dominate in different regions:

Source: WSJ Daily Shot as of 10/7/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.