U.S. Job Openings Drop 14% YoY, The Big Get Bigger, and the Velocity of Money Hits Six+ Decade Low

February 12, 2020 | FIRESIDE CHARTS

The number of U.S. job openings fell short of expectations to hit a two-year low in December, reigniting fears of a softening economy. This marks the second significant decline in a row and a 14% (1 million+) year-over-year drop. The S&P 500 may be continuing to reach new highs, but we’re fairly sure the state of the job market has the Fed’s (and Claudia Sahm’s) ears perked up. Mega-caps continue to be the driving force behind strong U.S. market performance with the S&P 500’s two largest companies, Apple and Microsoft, now comprising nearly 10% of the index. But you know what they say about putting all of your eggs in one basket… And while mega-cap market share is growing, the velocity of money in U.S. just hit a six+ decade low in a sign of slowing spending and—potentially—a contracting economy. Meanwhile, the coronavirus, now named COVID-19 by the WHO, continues to threaten economic growth. However, the Chinese market is rebounding on hopes of additional stimulus and some select commodities are on the rise; what will it take to sustain the trend?

1. Was December’s job openings count a bad print or the acceleration of the 10 month trend?

Source: WSJ Daily Shot, from 2/12/20

2. This is the year-over year data. Don’t forget the Sahm rule!

Source: WSJ Daily Shot, from 2/12/20

3. The big get bigger… What could possibly go wrong?

Source: WSJ Daily Shot, from 2/11/20

4. It is difficult at best to get robust inflation if the velocity of money is low…

Source: WSJ Daily Shot, from 2/11/20 & Investopedia

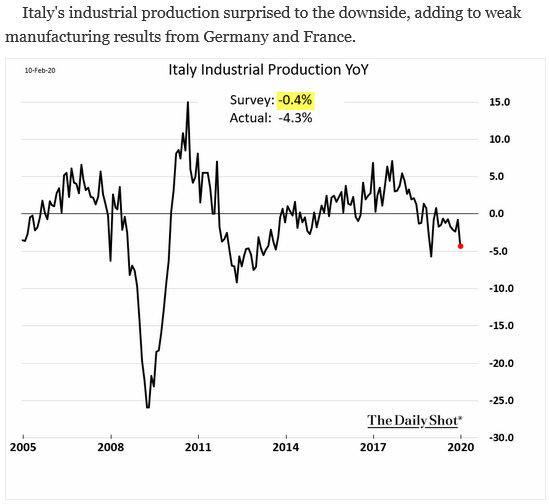

5. Europe cannot catch a break…

Source: JP Morgan, from 2/11/20

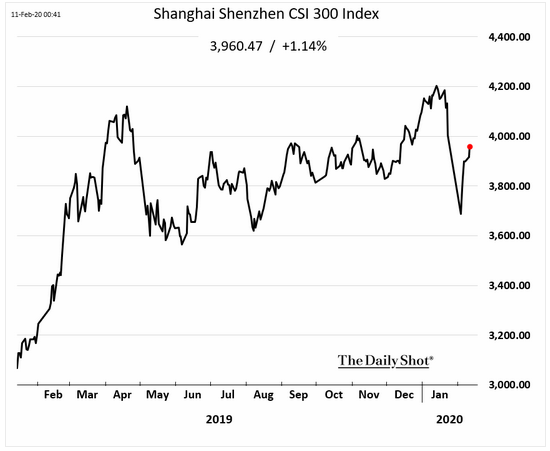

6. Will the Chinese stock market recovery continue?

Source: JP Morgan, from 2/11/20

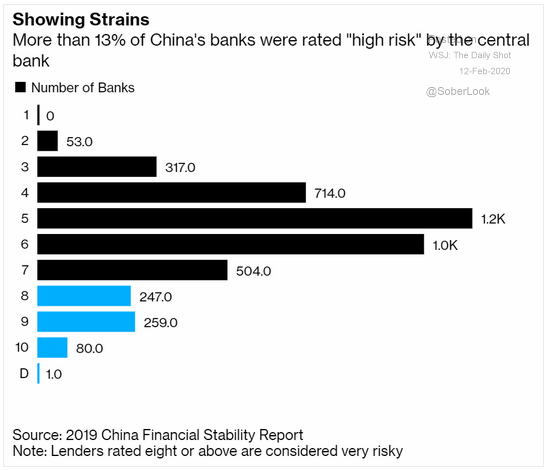

7. China’s growth has come with some growing pains; do they have their own financial crisis brewing?

Source: WSJ Daily Shot, from 2/12/20

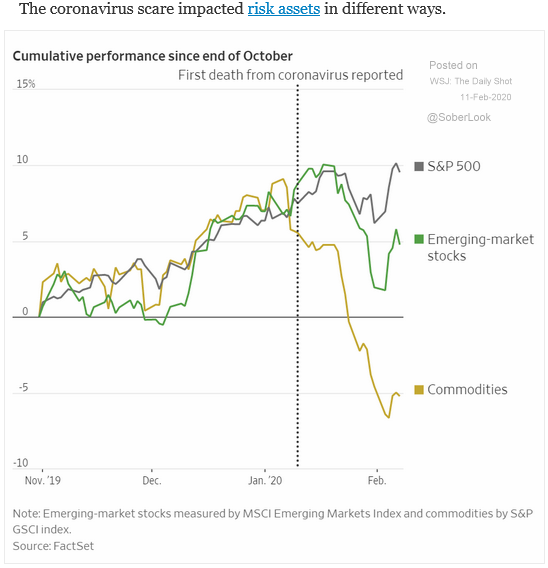

8. The trade wars and the coronavirus have decimated commodities. Are EM equities also a bargain?

Source: WSJ Daily Shot, from 2/11/20

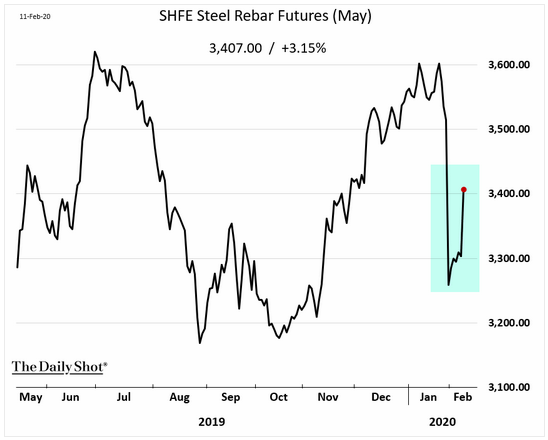

9. As the coronavirus fears are contained, many commodities, including Steel rebar in China, are rebounding….

Source: WSJ Daily Shot, from 2/11/20

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.