Retail Figures Beat Expectations, 30-Year Yield Hits All Time Low, and the Yield Curve Inverts

August 16, 2019 | FIRESIDE CHARTS

All eyes have been on the bond market this week as the 30-year U.S. Treasury yield sunk below 2% for the very first time, the 10-year yield hit its lowest point in three years, and the yield curve inverted. Sinking yields are a consequence of rising prices, meaning demand from worried investors—i.e. those looking for “safe” assets—is on the rise. How safe are bonds though when the global pool of negative-yielding debt is now approaching $17 trillion, up from last week’s high of $15 trillion? But beyond a recession—which nearly every platform (guilty!) has been hammering to death—what should you expect from equities and bonds following a yield curve inversion? And amidst all the angst, the announcement of July retail figures, which were stronger than expected, was welcome news. Consumer spending is typically viewed as the backbone of the U.S. economy and was largely responsible for Q2 GDP outperforming expectations. Expectations are still rising for three or more additional rate cuts in 2019 though, so we’ll be keeping our eyes out for any any news from the Fed as they release the minutes from the July meeting on Wednesday and gather in Jackson Hole on Thursday.

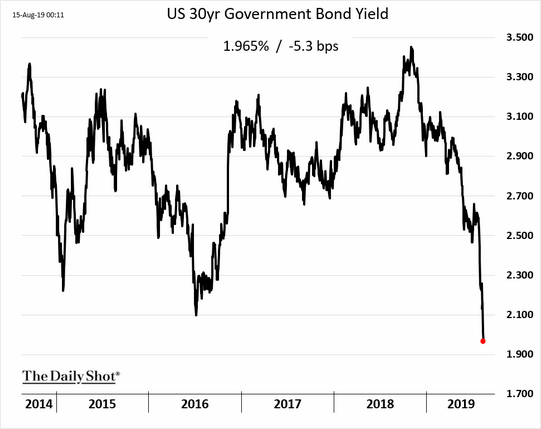

1. The 30-year Treasury yield fell below 2% for the first time ever.

Source: WSJ Daily Shot, as of 8/15/19

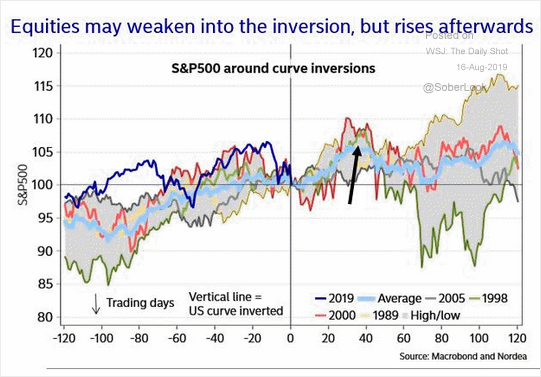

2. What should we expect following the yield curve inversion?

Source: Macrobond and Nordea, as of 8/16/19

3. And from equities?

Source: Macrobond and Nordea, as of 8/16/19

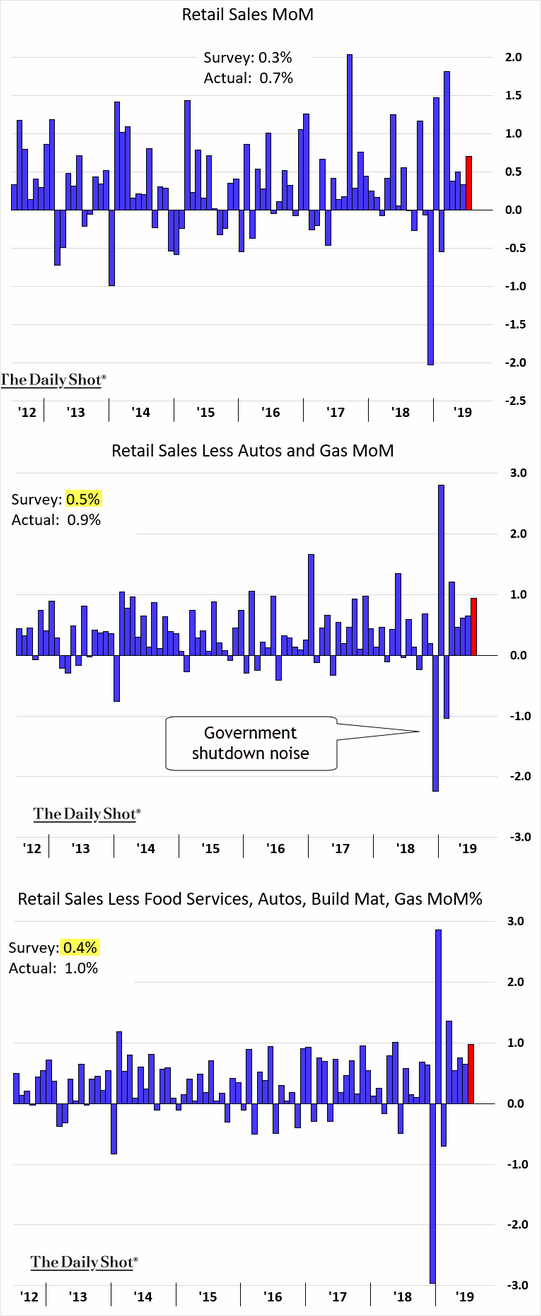

4. Retail figures outperformed expectations, soothing some anxiety for investors.

Source: WSJ Daily Shot, as of 8/1619

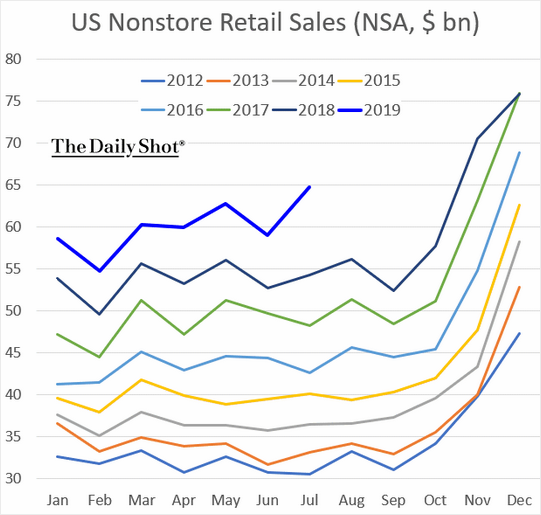

5. How much of the retail performance was thanks to July’s Amazon Prime Day?

Source: WSJ Daily Shot, as of 8/16/19

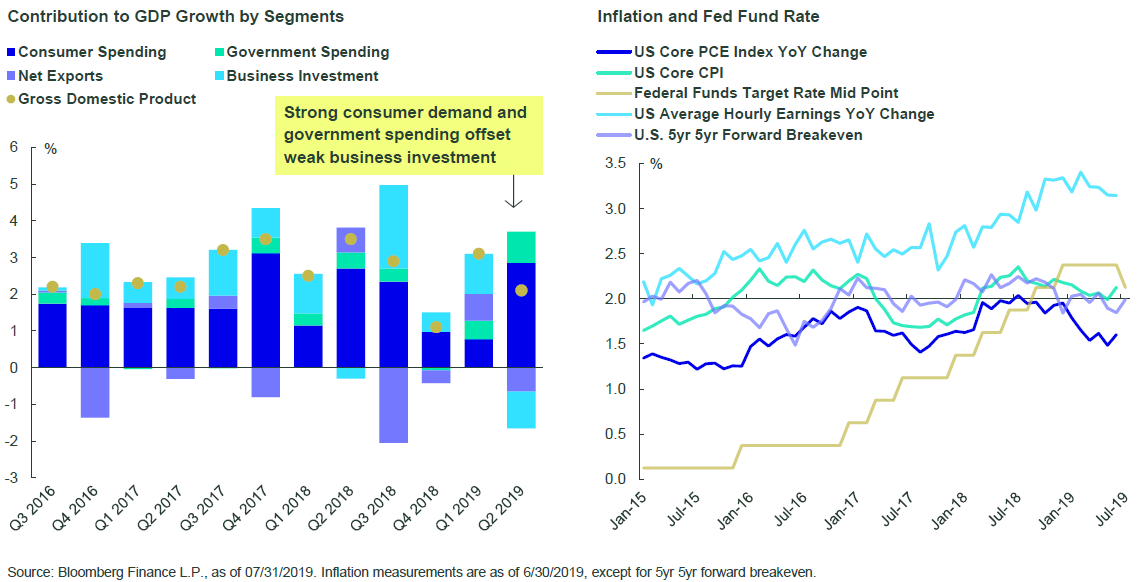

6. U.S. Q2 GDP also beat expectations, largely thanks to consumer spending. Could this, in addition to the Fed’s “insurance cut,” finally boost inflation?

Source: Bloomberg Finance, as of 7/31/19

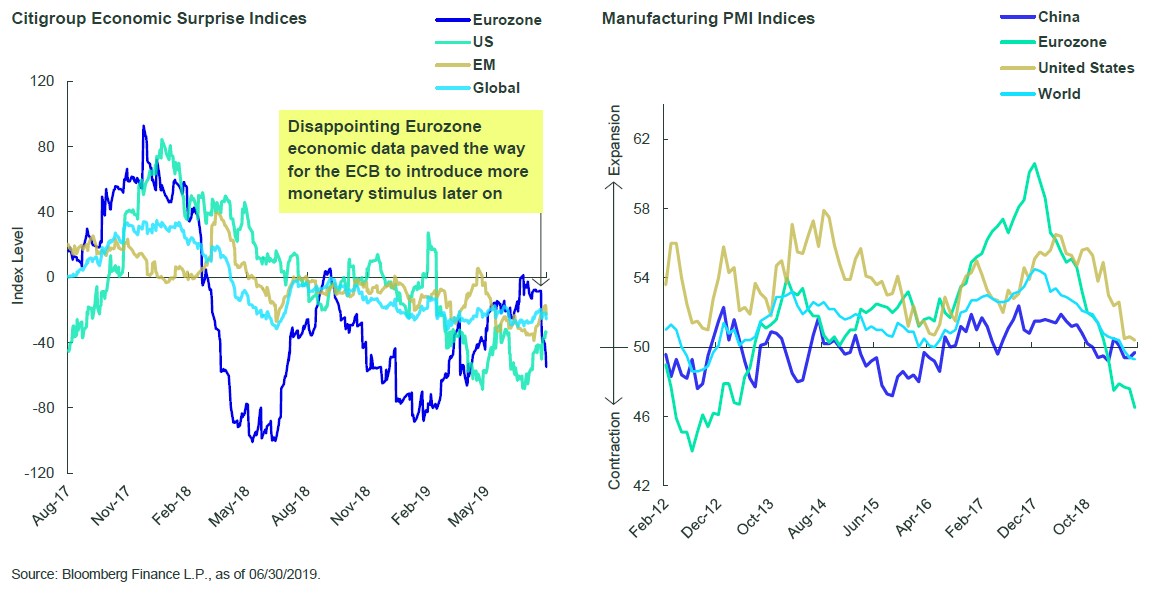

7. Despite this strong consumer demand in the U.S. though, global manufacturing weakness persists.

Source: Bloomberg Finance, as of 6/30/19

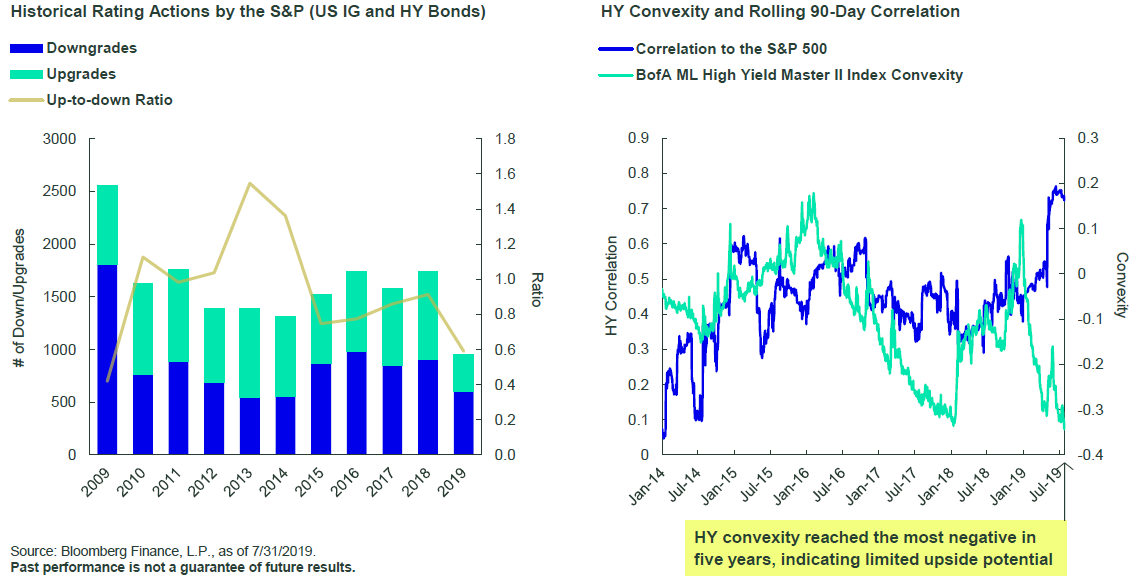

8. And we’re seeing a deterioration in credit quality, as well as historically high correlation between the high yield and equity markets.

Source: Bloomberg Finance, as of 7/31/19

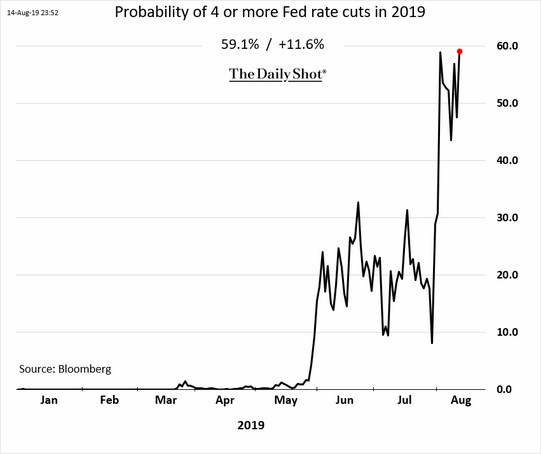

9. Could all of this mean we should expect several more rate cuts from the Fed in 2019? Economists seem to think so…

Source: WSJ Daily Shot, as of 8/15/19

10. Meanwhile, European banks are testing Eurozone debt crisis lows.

Source: WSJ Daily Shot, as of 8/14/19

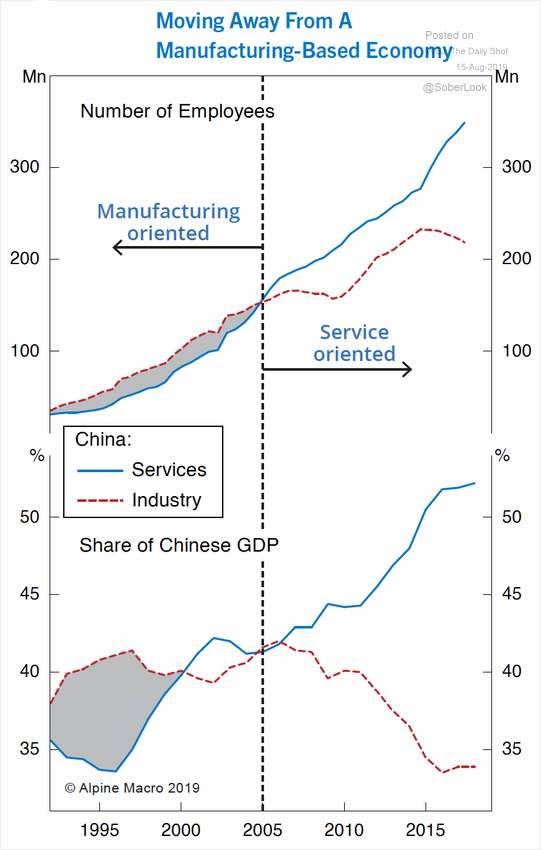

11. And finally, amidst the trade war, we’re seeing a shift in China’s economy. It seems their ultimate goal is to shift away from an export-dependent manufacturing economy towards a consumer goods and services oriented economy.

Source: Alpine Macro, as of 8/15/19

Disclosure: The charts and info-graphics contained in this blog are typically based on data obtained from 3rd parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be helf in client accounts.